TLDR

- Ribbon Finance is one of the top structured products protocols in DeFi, having $160m in TVL across their wide range of products - DeFi Options Vault (DOVs), R-EARN and undercollateralized lending (Ribbon Lend)

- Ribbon’s Theta Vaults (DOVs) serve as a passive strategy for users who are less familiar with options to still earn some yield from more complicated strategies

- Ribbon Treasury are customizable Theta Vaults (DOVs) that are focused on allowing DAOs to earn yield on native DAO tokens while diversifying and protecting the treasury value as yield earned can be paid out in many tokens such as USDC

- Ribbon recently launched two new primitives - R-EARN and Lend, which allows users to earn yield from lending USDC to market makers (MMs) (Wintermute & Folkvang). R-EARN offers 50% exposure of user’s deposits to each MM and uses part of the interest paid by MMs to purchase options to earn extra yield for users up to 20% APY. For Lend, users get to choose the MM they want to lend to, with yield being supported by interest paid by market makers and RBN emissions to offer 10-12% APY

- Aevo is the newest product under Ribbon’s ecosystem and aims to be the most liquid on-chain options DEX by directing volume in the DOVs to its order-book based DEX. The product is still under development but it aims to bring more sophisticated options strategies on-chain in addition to a margin system all on its own custom rollup. Early access to beta users is ongoing now with full public launch expected by the end of this year

Introduction

The options market in DeFi is still in its nascent stage. Based on Defillama, the options space has less than 50 protocols having a combined TVL of just $299m at the time of writing. Options are a subset of derivatives as the value of the contract is derived from the performance of an underlying asset, without the user having to actually buy or sell the asset itself.

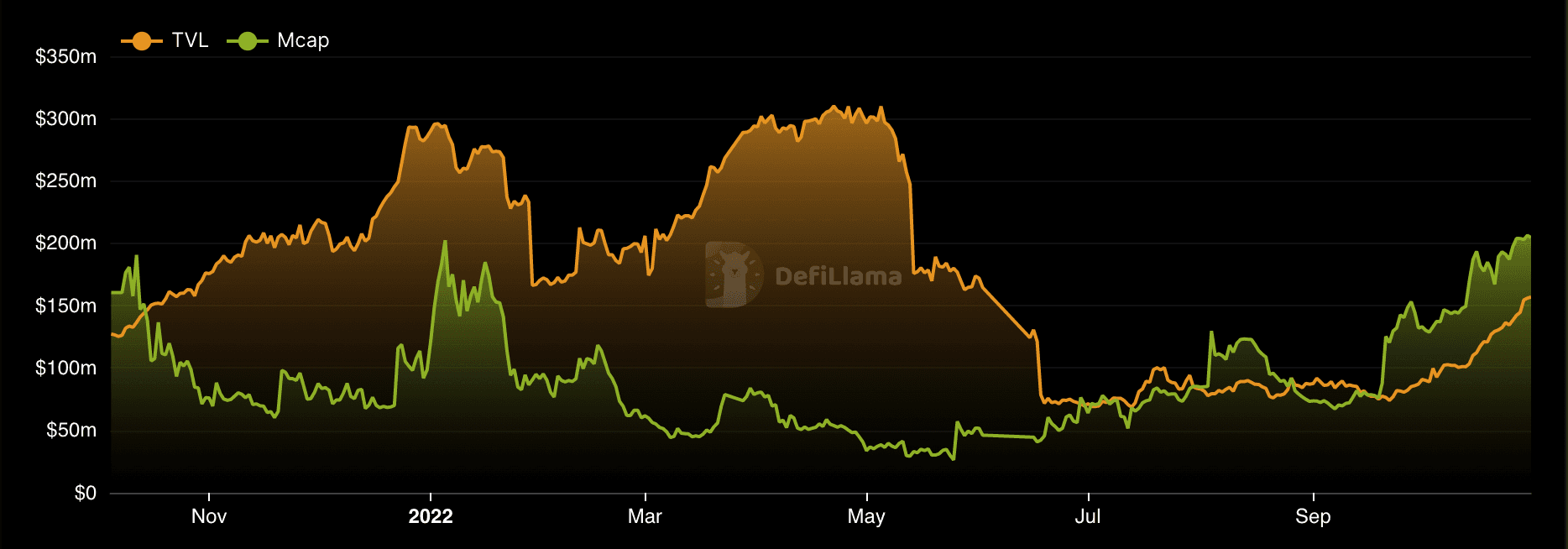

Ribbon Finance is a protocol offering DeFi structured products on Ethereum, Avalanche and Solana. Structured products offer other ways for users to earn yield in crypto, mostly by using derivatives that are often pre-packaged. Ribbon was one of the first protocols to offer DeFi Option Vaults (DOVs) on Ethereum with the launch of the Theta Vaults in April 2021. Since then, the vault has grown from just having under $20m in TVL in the first month to an ATH of around $300m within the year. Ribbon now offers a wider range of products, even delving into the lending market scene.

Products

Theta Vaults

Ribbon’s Theta vaults are essentially a passive strategy for users to earn yield through options without having to understand the strategy or executing the trades themselves. The vaults run on an automated European options selling strategy that carries out trades on behalf of all vault depositors weekly. Specific details on how the strategies are carried out for the Theta Vaults can be found here. The two main strategies are executed by writing out-of-the-money (OTM) options for both covered call selling and put selling. Strike price and expiration date selection are done through Ribbon’s model (based on the Black-Scholes model with adjustments), which focuses on volatility rather than the spot price of the asset. The yield generated from selling these options then goes back to depositors after taking into account a 2% management fee and 10% performance fee.

Ribbon forms the base layer where users interact with the protocol to deposit their funds while the actual execution of the contract (buying and selling options) is done on other protocols. Ribbon’s Theta Vaults currently utilize Opyn to execute options, making up over 80% of Opyn’s TVL.

Ribbon Treasury

The product was built for DAOs - with the strategy of earning yield by running covered calls on DAO native tokens. Unlike the Theta Vaults whereby strike price selection and frequency of execution are decided using Ribbon’s model, DAOs will get to set their own parameters for Ribbon Treasury. DAOs also get to decide on the type of token they want to receive the premium in, which also helps in diversifying the DAO treasury. The product is well suited to DAOs who do not actively trade their treasury funds, as they can put their tokens to work while being passive on the execution side. Ribbon takes a 10% fee on the yield earned, which is a win-win for both parties. Overall, the Ribbon Treasury product gives DAOs a lot of flexibility based on their risk profiles.

Perpetual Protocol was one of the first DAOs to be onboarded to Ribbon Treasury in February of this year. The initial deposit of 200k PERP (worth around ~$1m at that time) generated $17k in premiums in a month, equivalent to ~20.4% APY. The premium was paid out in USDC, which was beneficial for the DAO given that the token price of PERP has fallen by around 90% since then.

For Ribbon, their treasury product is a good B2B revenue stream that would likely be less reactive to market movements (eg. leaving for new protocols, market downtrend) as compared to retail users, which would help to mitigate the loss in revenue during a bearish market. It is also one of the first products focused on DAOs by accepting their native tokens for yield, allowing them to gain a competitive advantage in that aspect. In our research report on DAOs, the data has also shown that prominent DAOs have a large percentage of their treasury denominated in their own native token. Thus, diversification becomes crucial, especially in a downtrend whereby token prices have fallen significantly and treasury management became a larger concern for DAOs. Other than Perpetual Protocol, other partners of Ribbon Treasury include Balancer, Abracadabra and Badger DAO.

One key risk of Ribbon Treasury is counterparty risks, since market makers are needed to trade on the opposite side of the call options. The market makers onboarded for Ribbon’s Theta Vaults include QCP, Alameda, GSR and Wintermute, which would likely be the counterparties involved with Ribbon Treasury.

Ribbon Earn (R-EARN)

R-EARN was launched in August this year, and allows users to earn a yield of up to 20% by depositing USDC into the vault. This is aimed at users who are more risk-averse, especially in the current market whereby volatility of other collaterals supported on the DOVs may be too much to handle.

The yield mainly comes from interest on funds lent to market makers, Wintermute & Folkvang, which is currently set at 9.75% APR. Part of that interest (after excluding the base APY) is then used to buy weekly barrier options for ETH, options that expire worthless once it exceeds the barrier at expiry. The current barrier is set at 8% for both upside and downside from the strike price. Even if all options for that epoch expire worthless, users still get the 4% base APY. Ribbon takes a 15% fee on the yield earned between epochs, which excludes the 4% base APY. The vault operates on a 28 day epoch and any deposits/withdrawals within that timeframe will only take effect at the next epoch. Past performance on the vault shows that yield generated from the weekly barrier options is rather low (<1% APY), probably due to high volatility in the market that is hard to predict.

The product does come with risk even though it claims to be “principal protected”. Since users’ funds are not directly used to buy the weekly barrier options, the downside from options expiring worthless is mitigated while the upside potential is unlimited. However, users’ funds are fully dependent on the market makers not defaulting on their loans, which is a serious concern given the blackswan events that have happened in crypto this year. Furthermore, options that expire within the barriers may not be guaranteed yield if sellers do not fulfill their obligations to the vault. Smart contract risk is also a concern, as there has not been an audit on the vault.

Ribbon Lend

Ribbon Lend is similar to R-EARN as it allows users to deposit USDC to market makers of their choice, namely Wintermute or Folkvang, which was passed by a governance vote. Loans taken out by these market makers are undercollateralized, which is supposed to generate higher yield. One main differentiating factor that sets Ribbon Lend apart from its competitors is that they do not require lockups - which typically range from 90-180 days on other platforms.

Lend is currently supported by RBN emissions to be able to offer 10-12% APRs on the current pools. This is following a proposal to direct part of the 250k RBN emissions from the options vaults to Ribbon Lend to maintain a 5% RBN APR on Lend. It aims to incentivize users for Lend since the product is well-suited for the current market conditions since current emissions to the options vaults does not seem to be as effective as before, with TVL falling by half from ATH. The vote to implement the proposal passed with rather low margins, signaling that the move was highly contentious.

One downside of such liquidity mining programs is that it will tend to attract more mercenary capital who will “farm-dump” the reward tokens and leave once incentives stop, which harms both the protocol and the tokenholders. Similar to above, the main risk of the product would be the market makers defaulting on their loans or having insufficient capital to pay back the LP even though they have not “defaulted”.

Aevo

Aevo was created to expand the usage of DOVs to suit a wider range of traders, since the current DOVs on Ribbon only allow users to sell weekly OTM options. Aevo will be an orderbook-based DEX exchange that will include advanced options for traders, including choice of expiry dates and strike prices. The exchange is being built on a custom EVM rollup (an Optimism fork) which allows for easier onboarding from any EVM chain, lower fees and shared security from Ethereum.

Since DOVs are already a working product with a consistent stream of volume, all that will be directed to Aevo instead of leveraging other protocols like Opyn. This will ensure that Aevo will have sufficient liquidity - with the vaults having ~$78.0m and R-EARN having ~$12.7m. This is advantageous for Ribbon since it will generate more revenue and in turn benefit token holders if revenue share is turned on. Aevo will also deliver a better trading experience as users need not lock up their funds for a week in the vaults, since the orderbook will allow them to open or close positions at any time.

In the first Aevo AMA session, the team outlined that there are no plans to create a second token just for Aevo, hence, the product will be tied to RBN. The team also expressed the possibility of Aevo offering perps in the near future, which could allow for greater capital efficiency in terms of allowing for users to delta hedge by buying derivatives to mitigate exposure to direction of the options bought or sold. A lot remains to be seen as the team mentioned the focus on getting the launch right before introducing new mechanisms with the RBN token or possible revenue share. Nonetheless, the launch of Aevo will enhance the Ribbon ecosystem and push it towards being a major force in the structured products space.

Aevo is currently undergoing the beta testing stage, with full public launch slated to be by the end of the year.

Metrics

Ribbon has experienced significant growth in the past year, especially with the new product launches that helped boost its TVL to an ATH of ~$320m in late April. The increase could be attributed to the first liquidity mining program, which started in November 2021. veRBN was then introduced at the end of February, alongside boosted rewards and protocol revenue sharing as outlined in the proposal - which most likely contributed to the uptick from March. The launch of R-EARN in August and Lend in October did contribute to a slight increase in TVL at the initial stages. However, the overall slowing of market activity caused the adoption of these new products to be slower as compared to the launch of the Theta Vaults in 2021. Thus, a lower increase in TVL might not signify that these products are not good.

Meanwhile, the market cap of RBN has reached similar levels to the start of this year, despite RBN’s price being down 90% since then. This signals that RBN supply has been increasing significantly, which is set to continue further at the current stage of the supply schedule.

The number of users for Ribbon have been slowly increasing. Even during the launch of R-EARN and Lend, the number of new users being onboarded onto the platform only amounted to about 15-20 users a day, a far cry from the numbers last year. This could be part of the wider market slowdown whereby users are not actively looking for opportunities and not entirely a Ribbon issue.

Analyzing the performance of Ribbon’s products, DOVs utilization have slowed pretty significantly in the past few months. Particularly, the T-USDC-P-ETH pool saw a sharp decline of over 80% TVL from April to June, probably attributed to it being one of the worst performing vaults - having a negative cumulative yield of -24.7%. Another vault that is similar will be the T-AAVE-C vault, having -24.2% cumulative yield. The current best performing vaults will be the T-WBTC-C, T-STETH-C and T-ETH-C, with the cumulative yield ranging from 6-8%.

R-EARN currently has a TVL of 12.7m USDC out of the 25m USDC available. The usage is relatively small compared to DOVs. Particularly, for R-EARN, the top 5 depositors represent over 6.2m USDC, equivalent to 49% of the total vault deposits. This could signal that utilization of the product in terms of users is actually not that high even though the TVL has been increasing.

Ribbon Lend launched just under a month ago but has managed to attract over $69.3m in deposits at the time of writing. It currently offers slightly higher APRs (with RBN emissions) than protocols like Clearpool for the same counterparties, which could have contributed to it gaining traction. There is currently no fee structure in place, so Ribbon is not earning from Lend yet. However, if the growth of Lend continues, it could prove to be a lucrative and stable revenue stream for Ribbon.

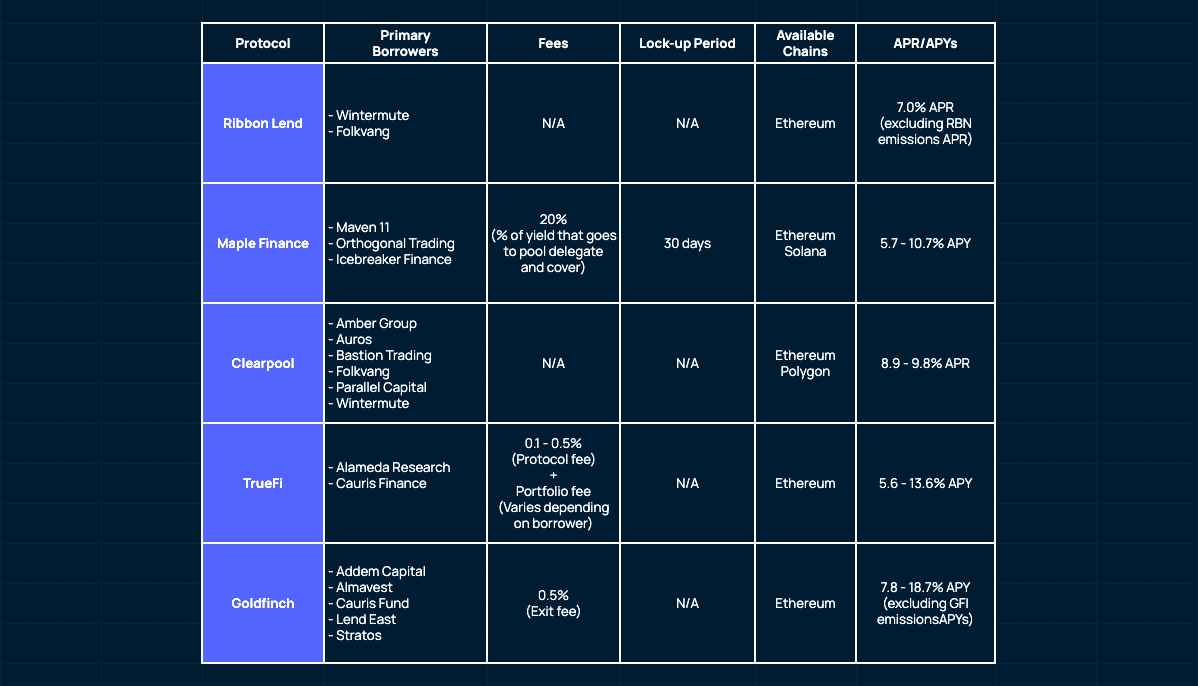

The table below shows a comparison between the different uncollateralized lending protocols - based on their borrowers, fees, lock-up period, available chains as well as yields.

*Clearpool’s yield is compounded at every block, hence, it is hard to give an estimate of true APY

Tokenomics

Users can choose to lock up their RBN for veRBN to get boosted RBN rewards on staking, bribes and share of protocol revenue. The locking model is similar to Curve whereby users receive veRBN based on the duration of locking - which ranges from 1 week to 2 years, and will decrease linearly till the unlock date. 50% of the protocol revenue is converted to ETH and distributed to veRBN holders, providing better cash flow than emissions in RBN.

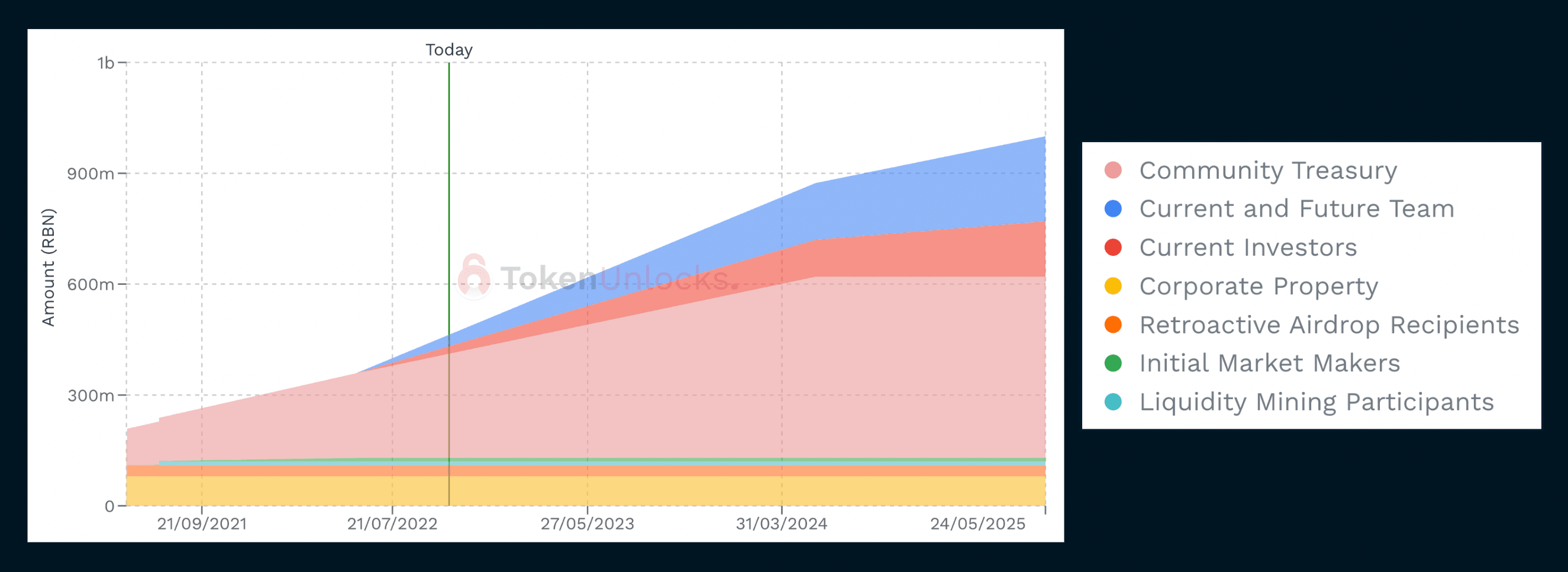

The total supply for RBN is 1,000,000,000. The breakdown for RBN’s token distribution are as follows:

| Category | Allocation |

|---|---|

| Community Treasury | 49% |

| Team | 23% |

| Private Investors | 15% |

| Corporate Property | 8% |

| Airdrop | 3% |

| LM Participants | 1% |

| Market Makers | 1% |

Source: Ribbon Finance

The current emission schedule for RBN is at its fastest, with the supply of RBN set to double by May 2024. Over 250k of RBN is emitted a week as incentives, which is equivalent to ~$84k at current prices. Given that the average revenue generated per week stands at ~$55k for the past 2 months, which means that the protocol is currently not in profit. There’s currently 35.9m RBN locked, which is 6.5% of the circulating supply. This is a rather low percentage as compared to protocols like Curve, which has an average of over 50% CRV locked. Hence, inflation is still a huge problem for Ribbon as holders are not incentivized to lock up their RBN for veRBN.

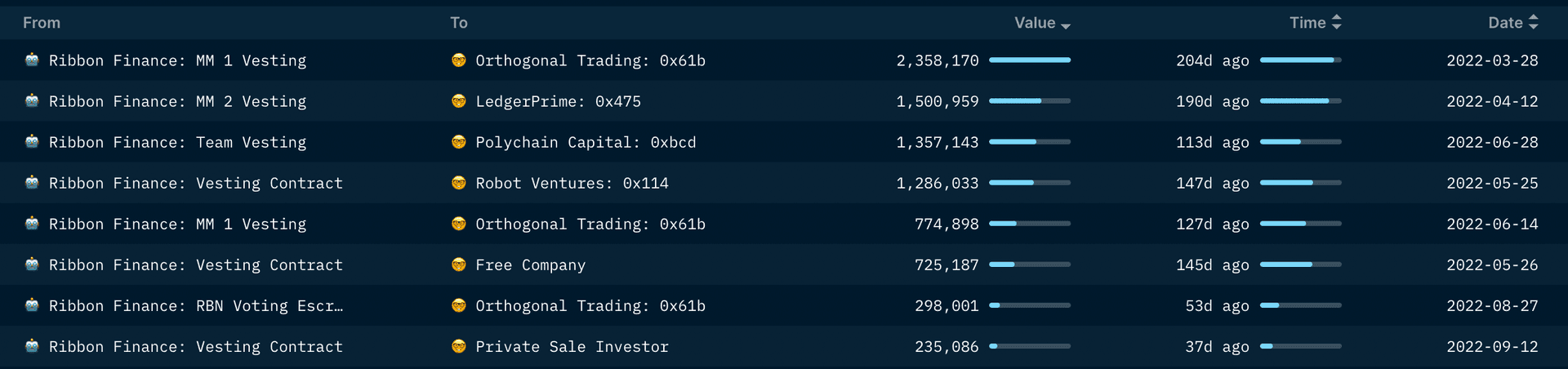

Ribbon had two funding rounds - a private round before the launch of the protocol and a recent $8.8m funding round in March led by Paradigm. Tokens for private investors follow a 1 year cliff followed by a 3 year vesting schedule starting from 24 May, 2021. The image below shows some of the Smart Money investors who have received their tokens from the Ribbon Finance vesting contract.

Based on the wallets who have received tokens from the vesting contract, we set up a Smart Alert to track the movement of these wallets with RBN tokens. These wallets (especially Smart Money) receive a significant amount of vested tokens and will be important to track when defending your position. Note that the list may not include all of the private investors of Ribbon Finance, as it is based on wallets that have already received tokens before the time of writing.

Overall, the inflation of RBN will be a cause for concern for most investors given that the current locking mechanism has not been as successful in reducing the amount of circulating supply. A possible catalyst for RBN will be when Aevo fully launches and the team announces how RBN can accrue value from the activity on Aevo. However, a lot still remains given more time is needed to analyze the performance of the newer products and how it could impact the Ribbon ecosystem.