1. 50 Shades of Gray

It is no surprise that following FTX’s Chapter 11 filing, market fears have shifted to Digital Currency Group (DCG). Both are among the largest “too-big-to-fail” empires within the cryptoverse.

While Barry was early to the game, starting DCG in 2015 (Grayscale in 2013) compared to SBF in late 2019, the trajectory of both in riding the crypto wave has been nothing short of spectacular. Now, the industry is nervously praying that any failure in the DCG empire will not be anywhere close to the one we just witnessed with FTX.

We are of the opinion that in contrast to FTX, DCG will survive this crisis. And while their portfolio might emerge significantly deflated, they will find a way to keep the group alive.

1.1 DCG Empire

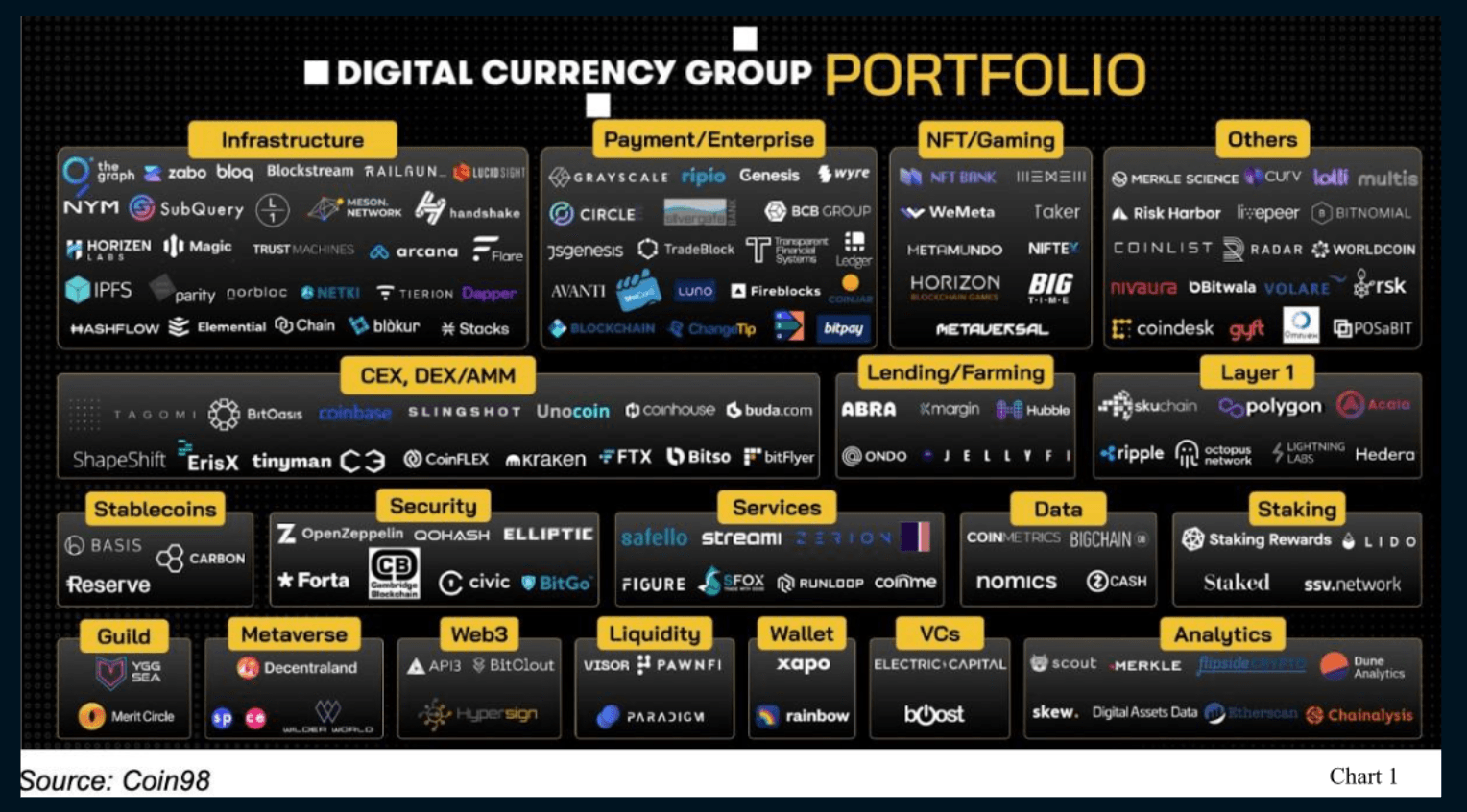

In 2015, DCG started with an AUM of just $25m, growing that to over $80bn AUM by the start of this year. Just like SBF, the web of its entity and investment list reaches every nook and cranny of the cryptoverse (Chart 1).

The crown jewels in this empire are Grayscale, Genesis Global Capital (Borrow/Lend), Genesis Trading (Broker/Dealer) and Coindesk.

Just like FTX, DCG was able to woo big name investors - raising $700m at a >$10bn valuation last November from names like Softbank and Alphabet’s VC fund CapitalG. Even a Singapore sovereign wealth fund has once again been involved, with Temasek’s bigger sister fund GIC also listed as an investor in that round.

However just like FTX, the massive growth and acquisitions on paper, which impressed these investors, were also fuelled by leverage, debt, and a rehypothecation model that centered around Grayscale and Genesis.

We’ve previously written about this rehypothecation model involving 3AC in our June quarterly edition of Just Crypto titled Zombieland

A crypto lender going belly up in this market, even a top institutional-grade one like Genesis, is arguably par for the course. However it is this rehypothecation between the parent DCG, Genesis and Grayscale which now threatens to drag the group down.

1.2 Genesis Global Capital

In his shareholder letter last week, Barry outlined the extent of DCG’s liabilities, which explains why DCG is doing everything it can to avoid Genesis filing for Chapter 11 bankruptcy.

Genesis is insolvent, with an urgent liquidity need of $1bn in capital to starve off bankruptcy.

However, DCG owes Genesis ~$575m in loans due May next year, loans which “were used to fund investment opportunities and repurchase DCG stock”... sound familiar?

In addition to these loans, there is another $1.1bn promissory note owed by DCG to Genesis with regard to the 3AC loan DCG took off Genesis books in June, due in June 2023.

If Genesis were to go into bankruptcy, then the liquidator would be calling on these loans, which DCG likely does not have the cash to repay right now.

So why can’t DCG pay Genesis back? This is because they still owe $350m in a credit facility to Eldrige, part of the $600m debt capital raise they did last November. Looks like somebody got too bullish right at the top.

Having said that, there is a major difference here compared to FTX. Going by the numbers Barry released, this looks to be more a liquidity issue rather than a solvency one. His $800m revenue number looks believable, and he seems to have much stickier capital.

A lot of DCG’s liquidity is stuck in illiquid assets which have value such as GBTC, rather than a bunch of pumped up shitcoins as per Alameda’s balance sheet. For example, in Q2, DCG took over 35m GBTC shares of collateral from 3AC (worth $316m mark-to-market (MTM) and $529m in NAV) in exchange for 3AC’s defaulted loan which they took off Genesis’ books.

There are also no DCG-originated tokens used to artificially inflate balance sheets and boost collateral against loans.

Finally, rather than commingled cold wallets in the case of FTX and Alameda, enabling easy shifting funds between one entity and the other, Grayscale’s assets sit in custody with Coinbase - a regulated entity who has verified the coin balance. On-chain forensics firm OXT Research has also independently estimated there are 634,639 BTC held in multiple GBTC related wallets, not far from GBTC’s 633,394 BTC number.

While many doubt this due to Grayscale’s refusal to submit their proof-of-reserves, there is a more rational, although no less damning, explanation for their refusal. Opening up their proof-of-reserves would allow many to track wallet transactions that could debunk Barry’s claim of “arm’s-length” dealings between Grayscale, Genesis and DCG, which might not have been at arm’s-length afterall.

However, all things considered, Barry has kept things much more kosher than SBF, although like so many crypto narratives this year, financial prudence in the face of greed has likely once again been found wanting.

This means that unlike SBF, there are still a number of ways out available to DCG which would allow them to survive this crisis - although many of these roads lead to their cash cow Grayscale.

1.3 Grayscale - The Sacrificial Cash Cow?

The story of Grayscale started with GBTC in September 2013. It was launched as a grantor trust, a structure akin to many gold ETFs like GLD. Like many other early crypto success stories, its success was built on being early into BTC - the once-in-a-generation wealth creator.

By being early, GBTC captured not just the exponential price increase, with the trust up 10,521% since inception even after a 71% decline this year, but more importantly, also the monopoly of the mass growth and adoption of the retail market.

We wrote about this in a telegram broadcast on GBTC in July last year during the raging bull market, and will not go into details here except to say that Grayscale, in particular GBTC and ETHE, have been massive cash cows for DCG.

At its peak last year, GBTC had an AUM of $60bn, which would have generated annual management fees for DCG of $1.2bn, for doing little other than ensuring custody! As expected, most of the work is done in the regulatory department, which is the main stumbling block for competitors looking to steal a share of this pie.

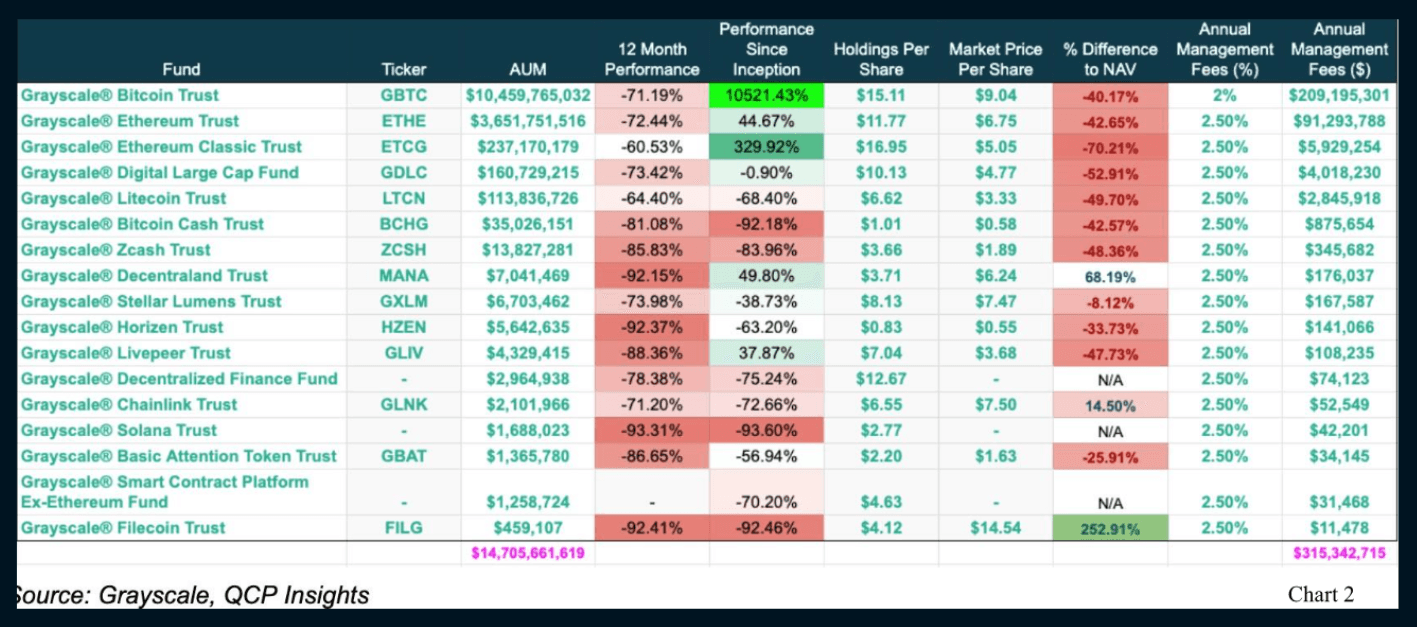

Even with today’s significantly smaller NAV, at 2% management fees on GBTC and 2.5% on ETHE and all other smaller trusts/funds, Grayscale is earning $315m per year in management fees alone just off the $14.7bn in combined AUM (Chart 2).

This is an amazing business model as management fees are collected off NAV, rather than market value. If we base this off MTM value instead, which most investment funds do, then Grayscale’s annual management fees are a whopping 3.6% for GBTC and 4.5% for ETHE respectively!

Previously, DCG was forced to buy-back large chunks of GBTC (of which they now own 9.67%) or ETHE (3.8%), and their only exposure was through collecting management fees - a great market-neutral model.

As Grayscale’s management fee coupons are clipped based on NAV, the size of their NAV (number of coins X value of coins) becomes more important than the market price of the shares themselves. The caveat being that these shares stay trading in premium, or nobody would want to create new shares in the trust themselves.

This is why the rehypothecation of loaning to large firms like 3AC and likely Alameda to subscribe new shares in order to boost NAV was so tempting.

This relationship extended beyond just BTC and ETH. In the last two or three years, Grayscale started launching trust after trust of altcoin after altcoin, for a total of 17 trusts/funds.

However replicating this model for the altcoin market did not get far following the implosion of the market this year. 10 out of 17 of these trusts/funds now have an AUM of <$10m. Furthermore, with all the trusts >$10m AUM all trading at significant discount currently, new subscriptions have totally dried up.

Which leaves us to speculate on game theory with Barry Silbert, and his search for liquidity.

A. Sell shares in open market

Even if DCG wanted to, there are regulations limiting them from dumping their shares on the pink sheets where GBTC trades.

Under SEC Rule 144(a), there is a clause which limits selling from affiliates.

“Trading Volume Formula. If you are an affiliate, the number of equity securities you may sell during any three-month period cannot exceed the greater of 1% of the outstanding shares of the same class being sold, or if the class is listed on a stock exchange, the greater of 1% or the average reported weekly trading volume during the four weeks preceding the filing of a notice of sale on Form 144. Over-the-counter stocks, including those quoted on the OTC Bulletin Board and the Pink Sheets, can only be sold using the 1% measurement.”

With the low average trading volume of just 83m shares a month, this means DCG can only sell a maximum of 6.9m shares every 3 months (1% of the 692.4m outstanding shares). At this rate, it may be too slow to raise the cash Barry needs.

It is possible that DCG has already been a seller in Q4, thus contributing to the widening discount. However we will only know for sure at the Q4 filing date sometime in February next year.

B. Liquidate Trust

The MTM value of DCG’s GBTC and ETHE position is $625m, with an NAV of about $1.1bn. This means liquidating the trust will immediately unlock $469m in value for them, ceteris paribus.

However, compared to the management fees they could potentially collect for years to come, this seems like pittance. This year, even in today’s depressed markets, DCGT is looking at $300m in fees this year alone, following close to $1bn last year at its peak.

Hence, one can bet that voluntary liquidation of the trust by DCG will not be forthcoming - but can they be forced into it?

There can be no doubt many GBTC shareholders or activist investors would be eyeing liquidation of the trust to unlock the inherent NAV value.

Grayscale seems to have anticipated this possibility of others coming to steal their cash cow, by changing the language in the Voting and Approvals section of the filing in order to prevent this from potentially happening.

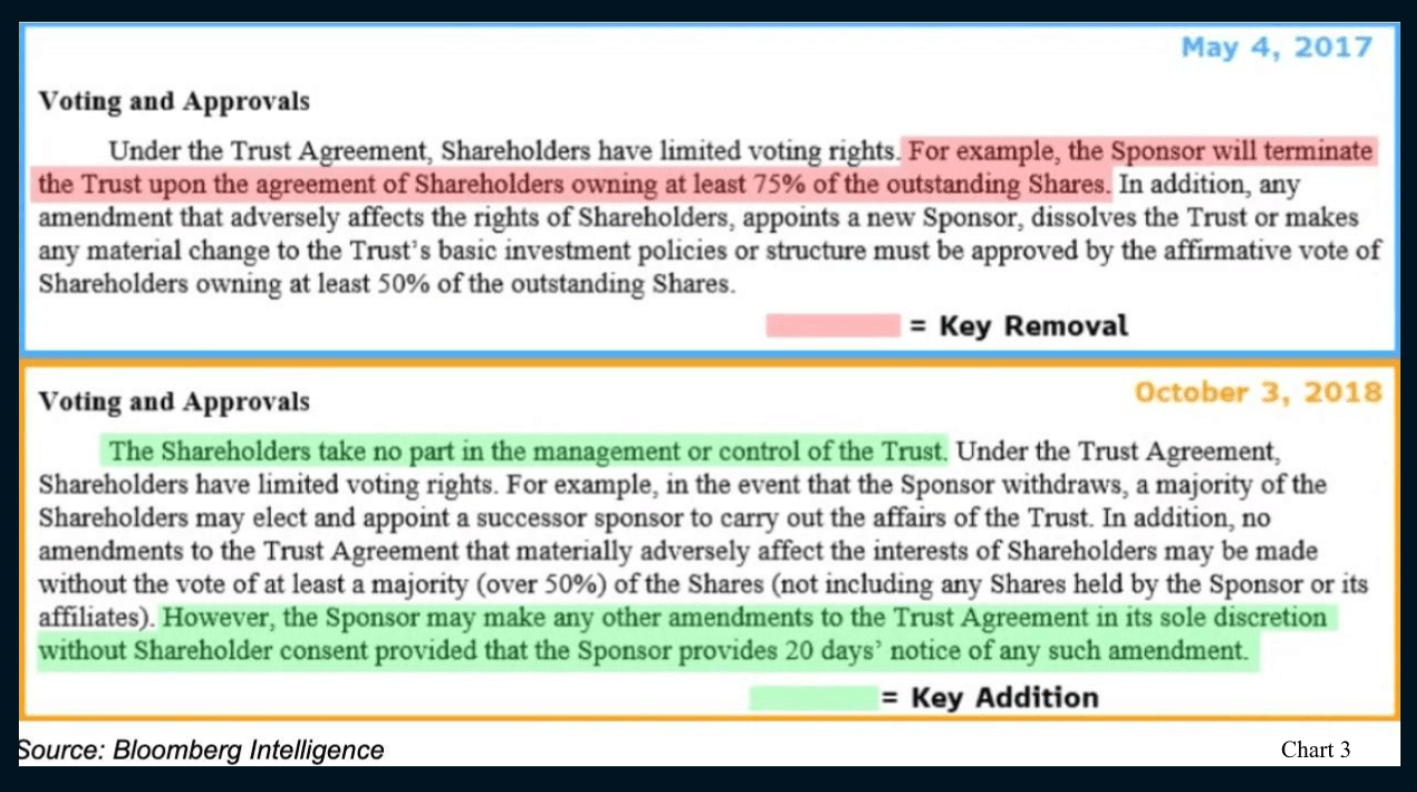

GBTC filings from May 2017 had language that allowed for liquidation of the trust if 75% of shareholders agreed to the termination, but in the following filing in October 2018, and all subsequent ones since, this looks to have been removed altogether (Chart 3).

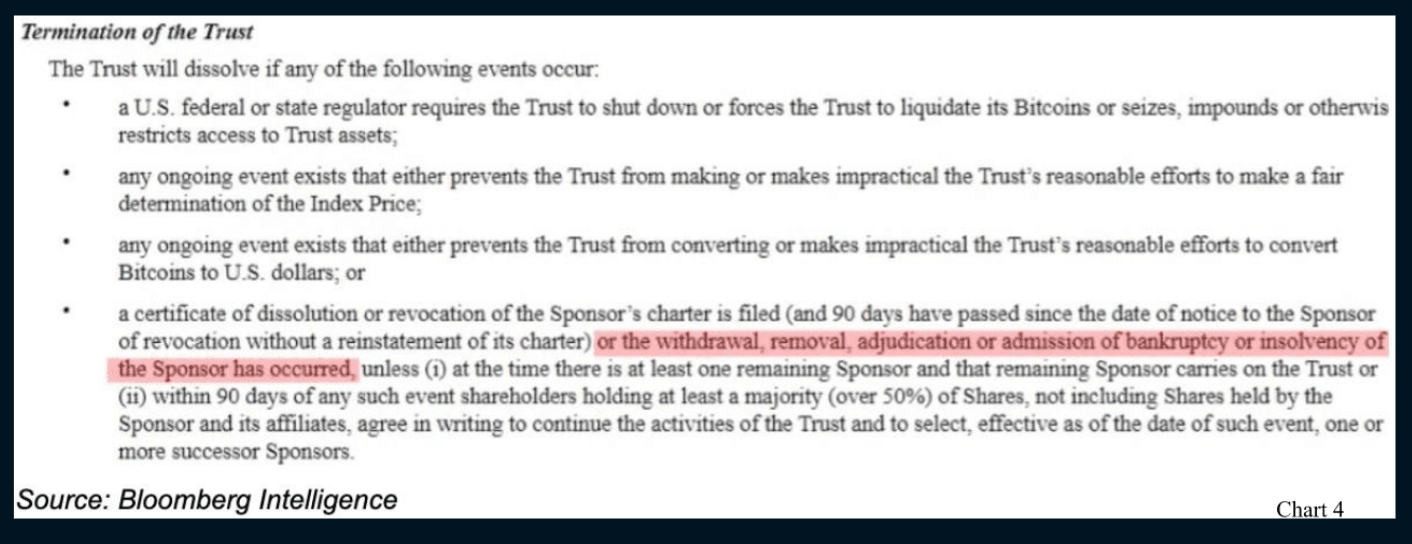

Apart from proxy voting, GBTC filings also state that insolvency or bankruptcy of the trust’s sponsor (Grayscale) would constitute a reason for liquidation of the trust, unless 50% of shares in the trust vote to transfer to a new sponsor (Chart 4). Thus any bankruptcy to DCG, something we do not foresee, would ultimately also lead to liquidation of the trusts, unless they find a new sponsor.

Grayscale seems to have anticipated this possibility of others coming to steal their cash cow, by changing the language in the Voting and Approvals section of the filing in order to prevent this from potentially happening.

GBTC filings from May 2017 had language that allowed for liquidation of the trust if 75% of shareholders agreed to the termination, but in the following filing in October 2018, and all subsequent ones since, this looks to have been removed altogether (Chart 3).

At this point, if any liquidation were to occur, cash will be returned to investors, as Grayscale has stated in its filings.

"If the Trust is forced to liquidate, the Trust will be liquidated under the Sponsor’s direction. The Sponsor, on behalf of the Trust, will engage directly with Bitcoin Markets to liquidate the Trust’s Bitcoin as promptly as possible while obtaining the best fair value possible."

We suspect that if this comes to pass, perhaps an option would be written in for large shareholders to have the option to receive coin instead, in order to minimize the massive market impact of selling more than 633k BTC, 3.1m ETH, 11m ETHC etc, not to mention the impact the front-running of these flows will have.

In any case, GBTC is very much a retail product. The largest institutional holders own only 11.18% of GBTC’s outstanding shares - with DCG accounting for 9.67% alone (Chart 5). The rest of GBTC shares are owned by over 850,000 account holders.

Faced with these choices, it is also no wonder that Grayscale has been pushing so hard for an ETF approval, even suing the SEC in the process. At this point, this no doubt looks to be the best option for them and the market as well, even if this means a massive haircut to their 2-2.5% management fee model.

1.4 Where to from here?

With the Mt. Gox liquidation also looking to reach a resolution next year, which would finally see its creditors paid 141,686 in BTC, we could see the market continue front-running these potential selling flows into the new year. Small consolation in the case of Mt Gox, creditors have been given a choice between either receiving BTC, or cash “at a much later date”.

Thus we believe that while more one-off shocks might not be so forthcoming in a market filled with fear, a continued deflation of the crypto market will continue well into next year as many are forced to continually sell assets to raise liquidity.

This will likely only end in late Q2-Q3 next year when the real economy gets badly hit from the 4.75% overnight rate and the Fed is then forced to pivot - releasing much needed liquidity which could then find its way into crypto markets once again.

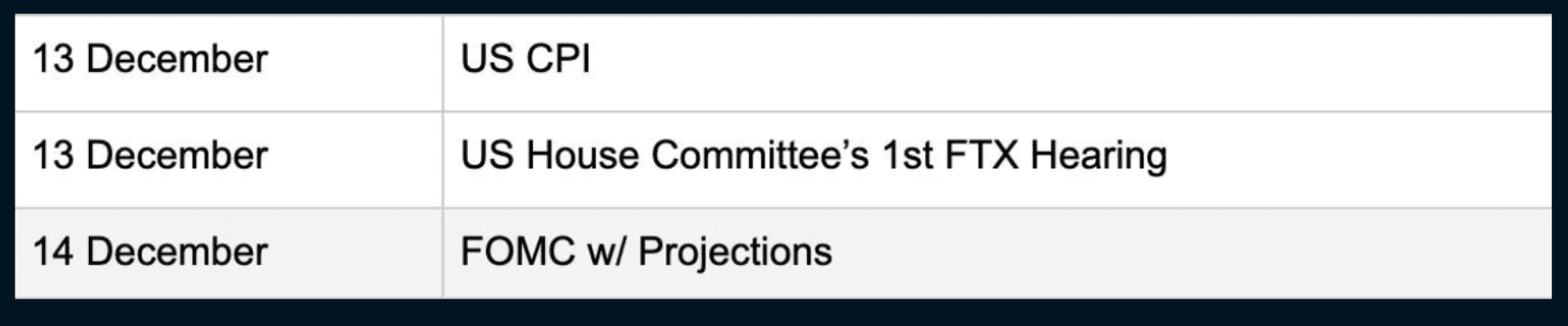

2. Upcoming Risk Events

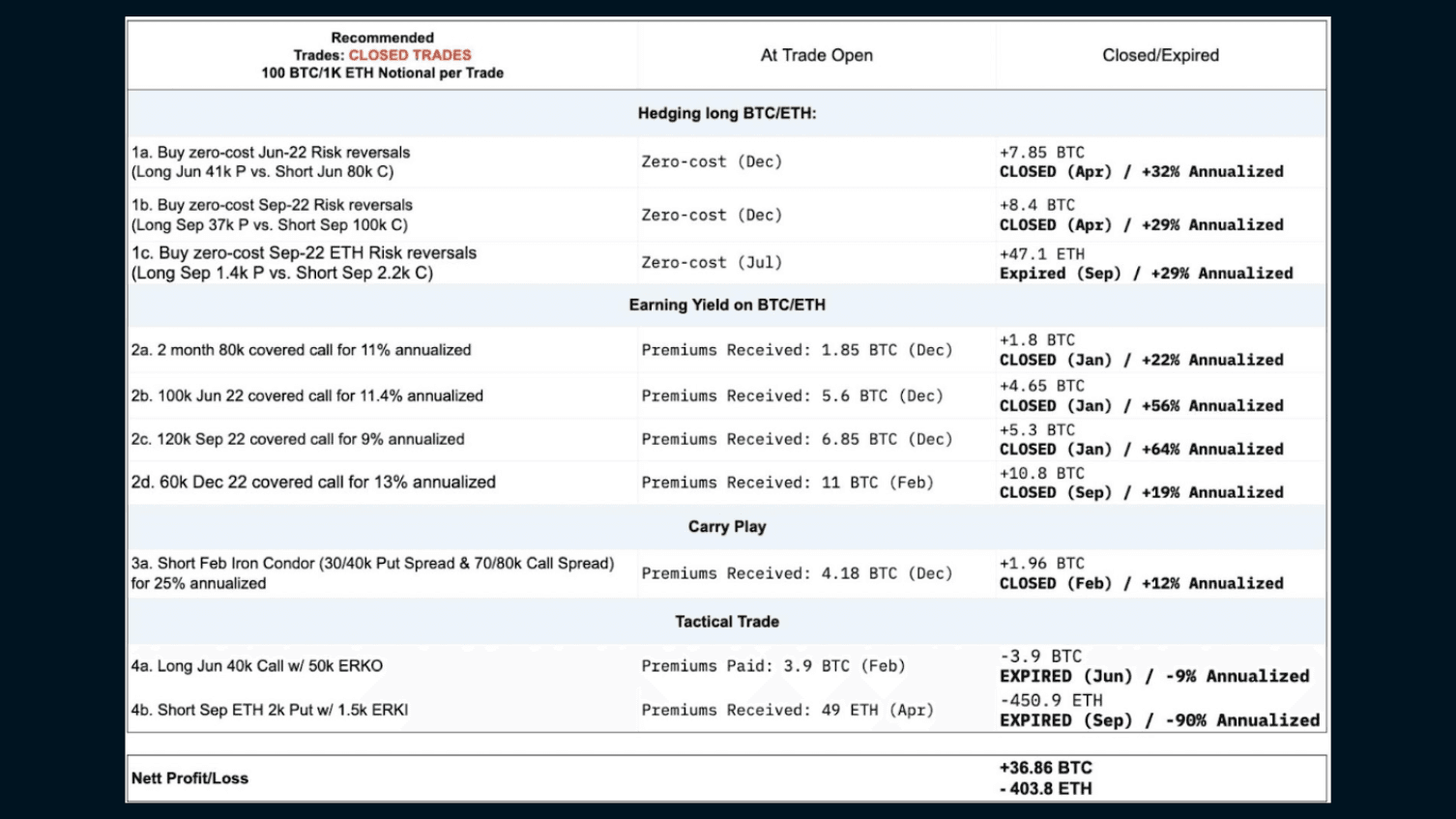

3. Trades Update

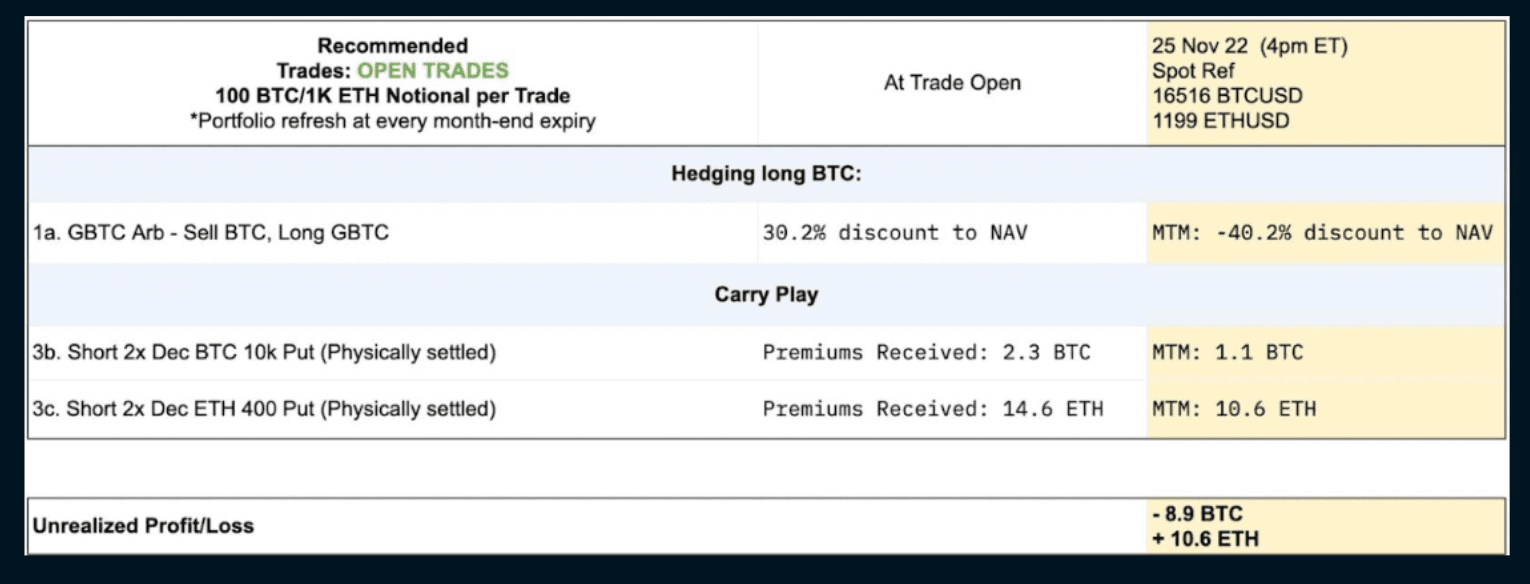

Next month, our final two open option positions will expire and we will close out the book for the year, only carrying over the GBTC arbitrage trade into next year.

That trade has not been working, in addition to the negative carry. However at the same time, closing out this trade now would synthetically imply selling BTC at $9,800 (the market price of GBTC’s BTC now), and that just doesn’t sit right with us.

In fact, on 21 Nov GBTC's discount reached 50% intraday - equivalent to buying BTC at $7,900 while spot was trading at $15,800. For those who believe in the potential of BTC, this instead looks like a great contrarian outright buying opportunity.

Finally, similar to last December’s Just Crypto: 2021 Review & 2022 Outlook, next month’s year-end Just Crypto piece will feature a 2022 recap and 2023 outlook, along with how we will be positioning the book going into the new year. Keep a look out for that!

Disclaimer

QCP Capital is an exempt payment services provider pending licensing by the Monetary Authority of Singapore as an MPI for Digital Payment Token Services under the Payment Services Act (2019).

This information contained in this document is intended as a general introduction to QCP Capital and its activities as a Digital Payment Token (DPT) service provider and is for informational purposes only. QCP Capital is not acting and does not purport to act in any way as an advisor or in a fiduciary capacity vis-a-vis any counterparty. Therefore, it is strongly suggested that any prospective counterparty obtain independent advice in relation to any trading investment, financial, legal, tax, accounting or regulatory issues discussed herein. This document is only directed at informed and qualified investors. By reading this material attests that you are fully aware that trading of DPTs is not suitable for the general public and that you are an informed and qualified investor, and are also fully cognisant of all technological and financial risk(s) associated with trading Digital Payment Tokens.

Before you engage us or any of our services, you should be aware of the following:

QCP Capital is an exempt payment services provider pending licensing by the Monetary Authority of Singapore as an MPI for Digital Payment Token Services under the Payment Services Act (2019). Please note that this does not mean you will be able to recover all the money or DPTs you paid to your DPT service provider if your DPT Service Provider’s business fails.

You should be aware that the value of DPTs may fluctuate greatly. You should buy DPTs only if you are prepared to accept the risk of losing all of the money you put into such tokens.

You should not transact in the DPT if you are not familiar with this DPT. This includes how the DPT is created, and how the DPT you intend to transact is transferred or held by your DPT service provider.

You should be aware that your DPT service provider, as part of its licence to provide DPT services, may offer services related to DPTs which are promoted as having a stable value, commonly known as “stablecoin”.