Introduction

With the Shanghai upgrade fast approaching, and the LSD narrative in full flow, this report looks at what effect Shanghai will have on ETH (un)staking and the potential post-Shanghai selling pressure. There are currently two trains of thought;

- Shanghai will result in significant sell pressure as large amounts of locked ETH become available to sell and

- Shanghai is bullish, and will have a low overall impact on ETH selling pressure.

This report assesses a likely outcome of the Shanghai upgrade by covering:

- A Shanghai recap including an overview of the Shanghai upgrade and current staking statistics as well as an explanation of the withdrawal process.

- A scenario for unstaking-based selling pressure by clustering stakers into groups and predicting their actions (i.e. likelihood to sell) post Shanghai.

- Other factors to consider that may affect buying/selling pressure.

- Spot volume and liquidity in order to put the selling pressure in perspective.

Current Staking Statistics

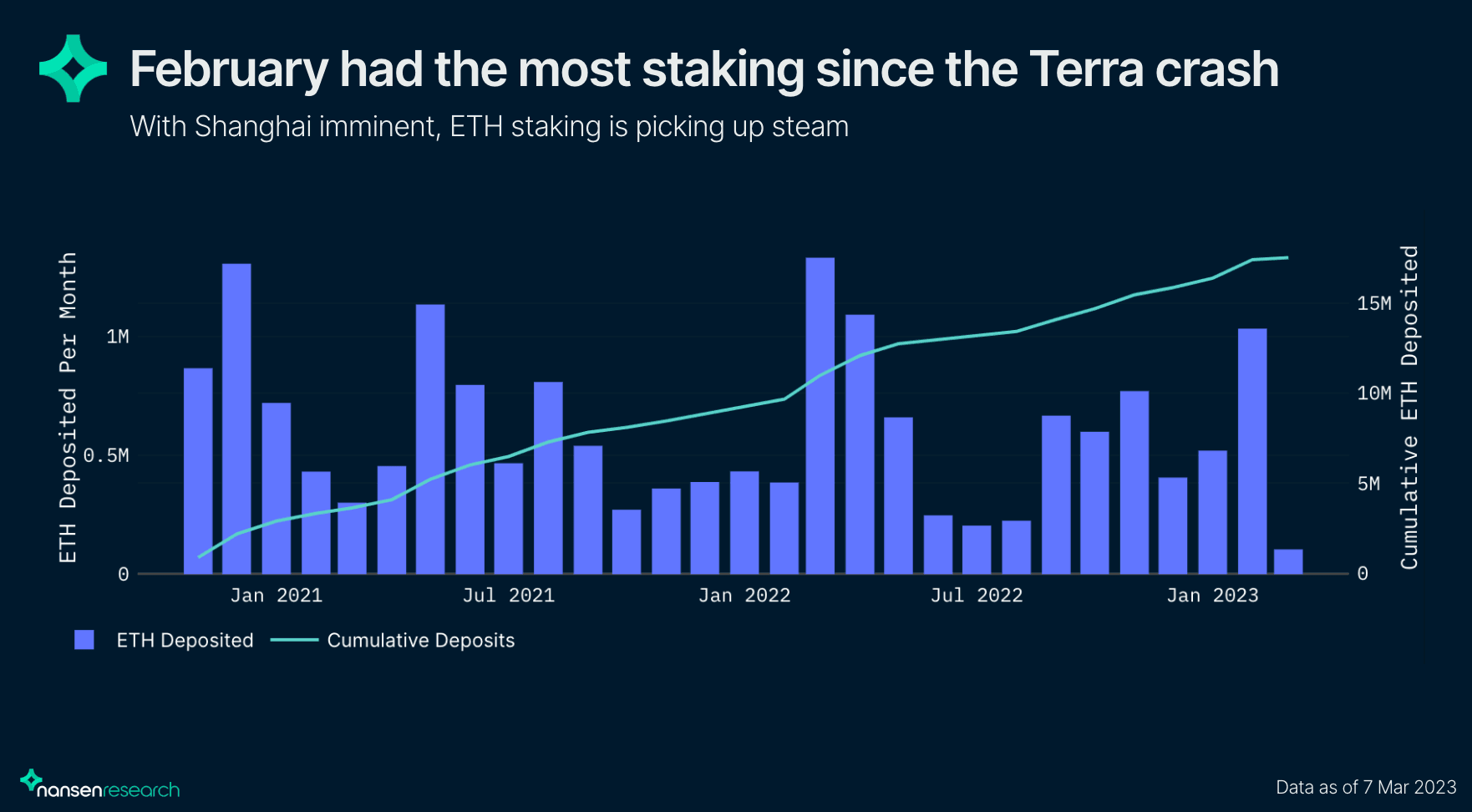

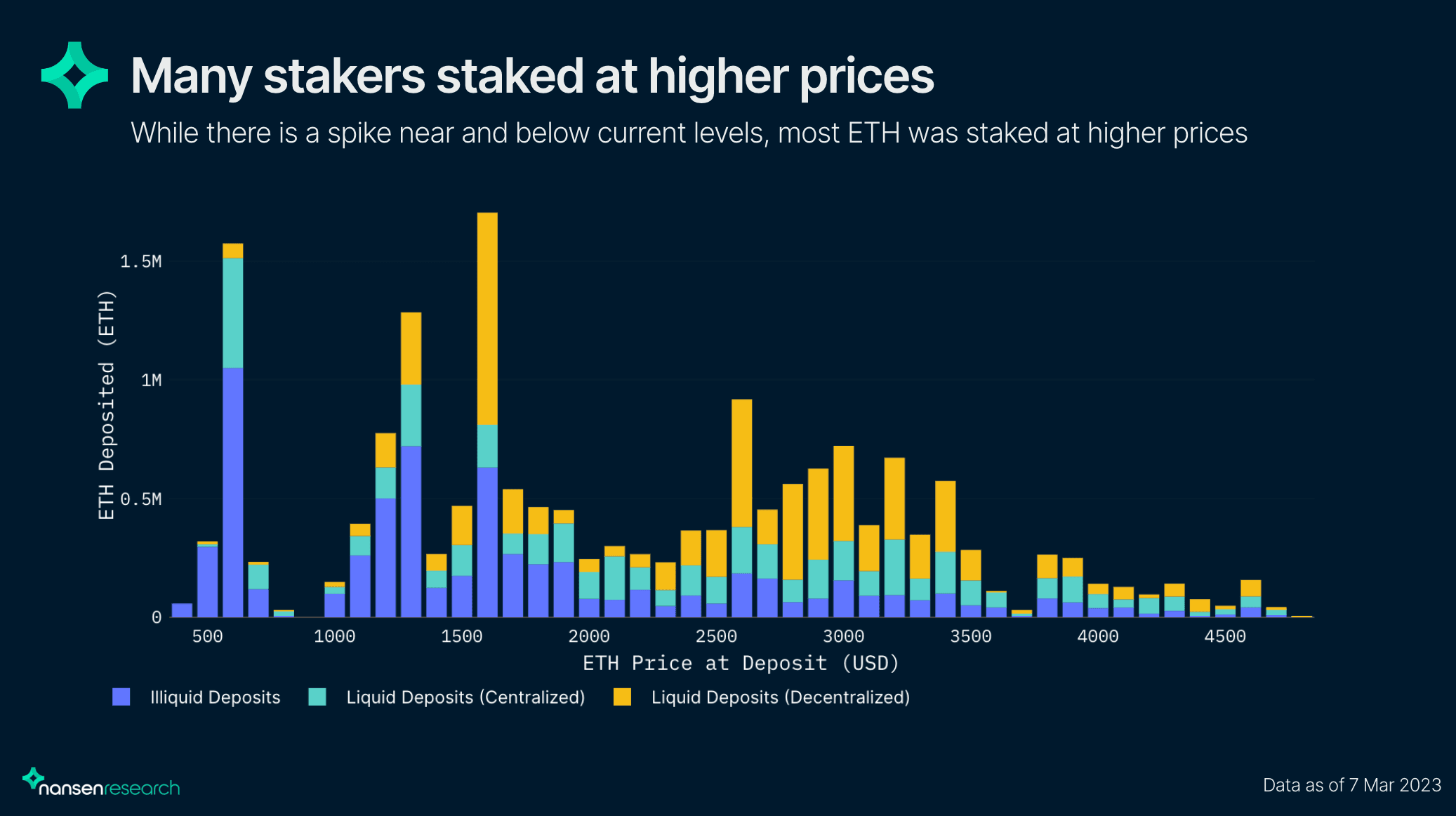

With Shanghai around the corner, ETH staking is going strong. February was the busiest month since the crash in June, including a massive 150k ETH deposit from Justin Sun into Lido. Around 17.5m ETH has been deposited - over 14% of the total supply.

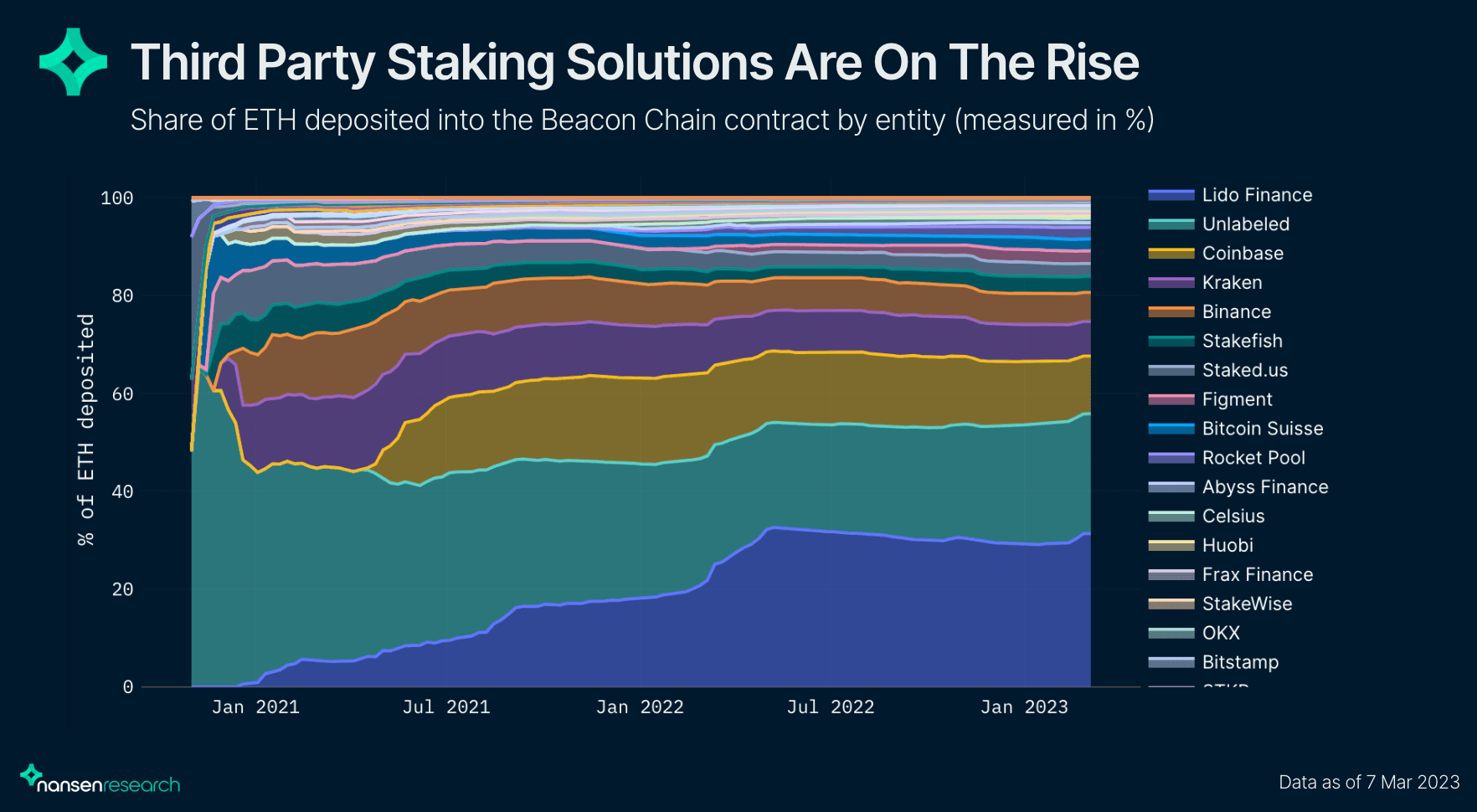

Most deposits can be attributed to a few large entities. With Lido leading (31%), followed by Coinbase, Binance and Kraken (collectively 24.7%), the majority of staked ETH (62%) is with liquid staking providers. The big category of unlabeled depositors are depositors unknown to Nansen and are assumed to fall into the category of illiquid stakers.

If you want to monitor beacon chain deposits yourself, check out our live ETH2 dashboards as well!

Shanghai Recap

To become a validator in Ethereum’s PoS Beacon Chain and earn staking rewards, it is necessary to stake 32 ETH. Only these 32 ETH earn rewards, with no auto-compounding. The caveat was that staked ETH would be locked until after The Merge, which has successfully occurred. The Shanghai Upgrade is a hard fork that will enable withdrawals of ETH. The withdrawal process will not occur all at once, but participants will have a timeline and path to unstake (and sell!) if they wish. Shanghai is expected in early to mid-April, pending a successful upgrade to the Goerli network on the 14th of March.

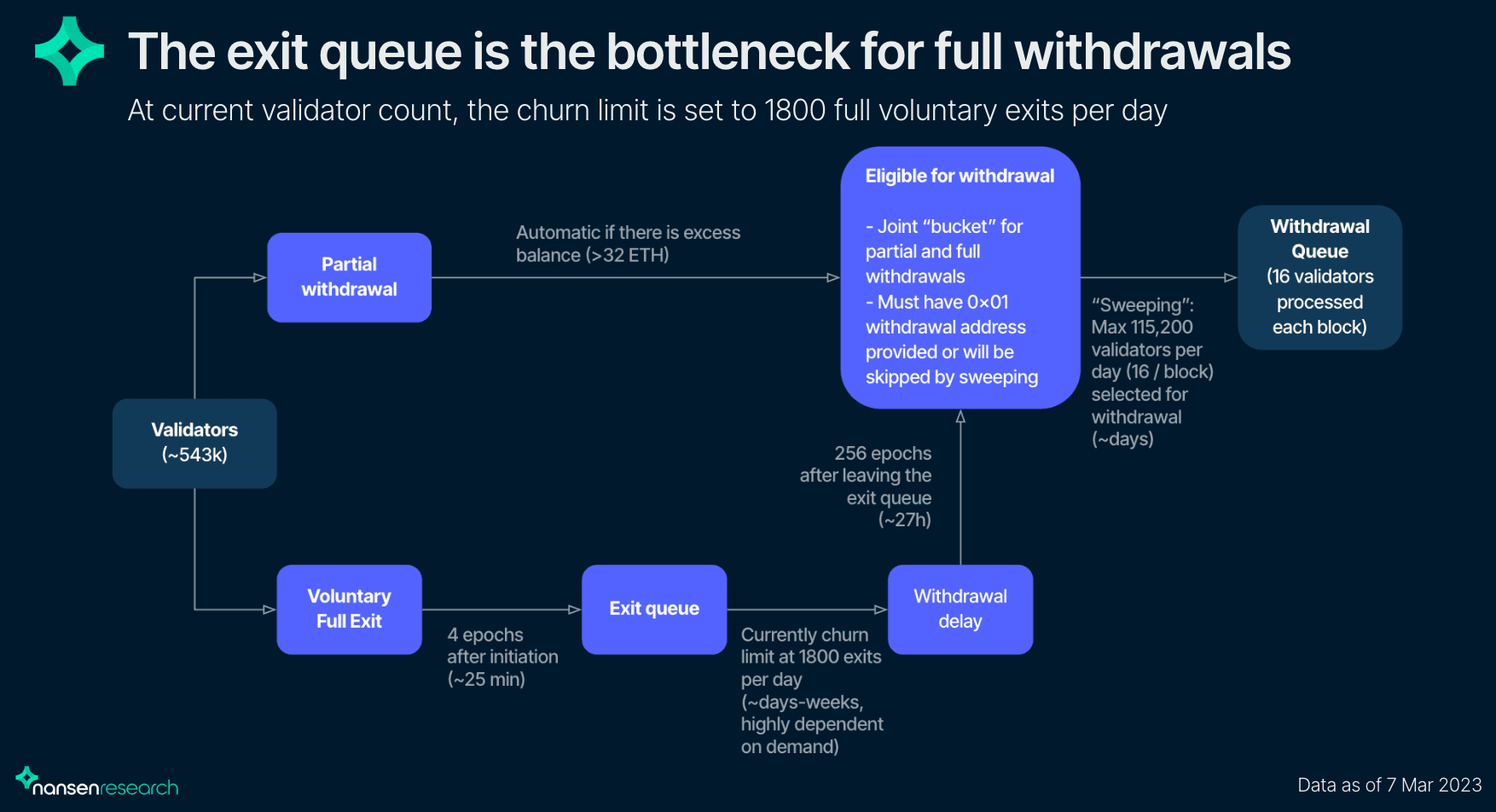

Stakers will be able to trigger either a partial withdrawal or full withdrawal of funds. Partial withdrawals will be made available for withdrawal first, whereas full withdrawals have to go through an exit process that will take additional time.

The current block proposer “sweeps” through all validators eligible for withdrawal. It starts at the validator index where the last proposer left off, and selects the first 16 eligible validators for the withdrawal queue. This withdrawal queue is then processed in the current block. Note that in order to withdraw and/or receive rewards, users need to update their withdrawal address to the 0x01 format. As of 7 Feb 2023, more than 50% of validators are yet to complete this, and if they do not do so before Shanghai they will not be able to withdraw (until they do so).

Partial Withdrawals

This allows validators to withdraw any “excess balance” over 32 ETH, predominantly accrued rewards. If the validator has updated the withdrawal address to the 0x01 format this will happen automatically and could theoretically happen immediately, although in most cases it might take some days to make it through the withdrawal queue and be processed. Partial withdrawals, i.e. distribution of rewards, are expected to happen around every 5 days (assuming ~600k validators).

Full Voluntary Exits

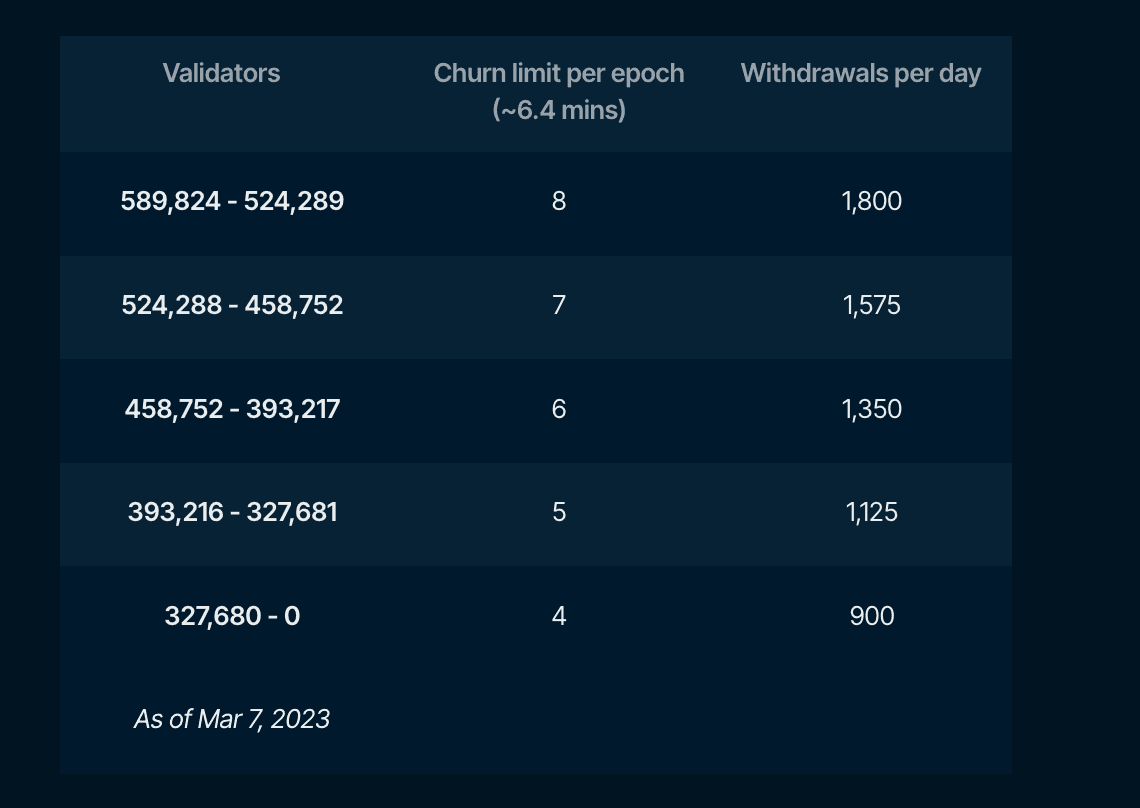

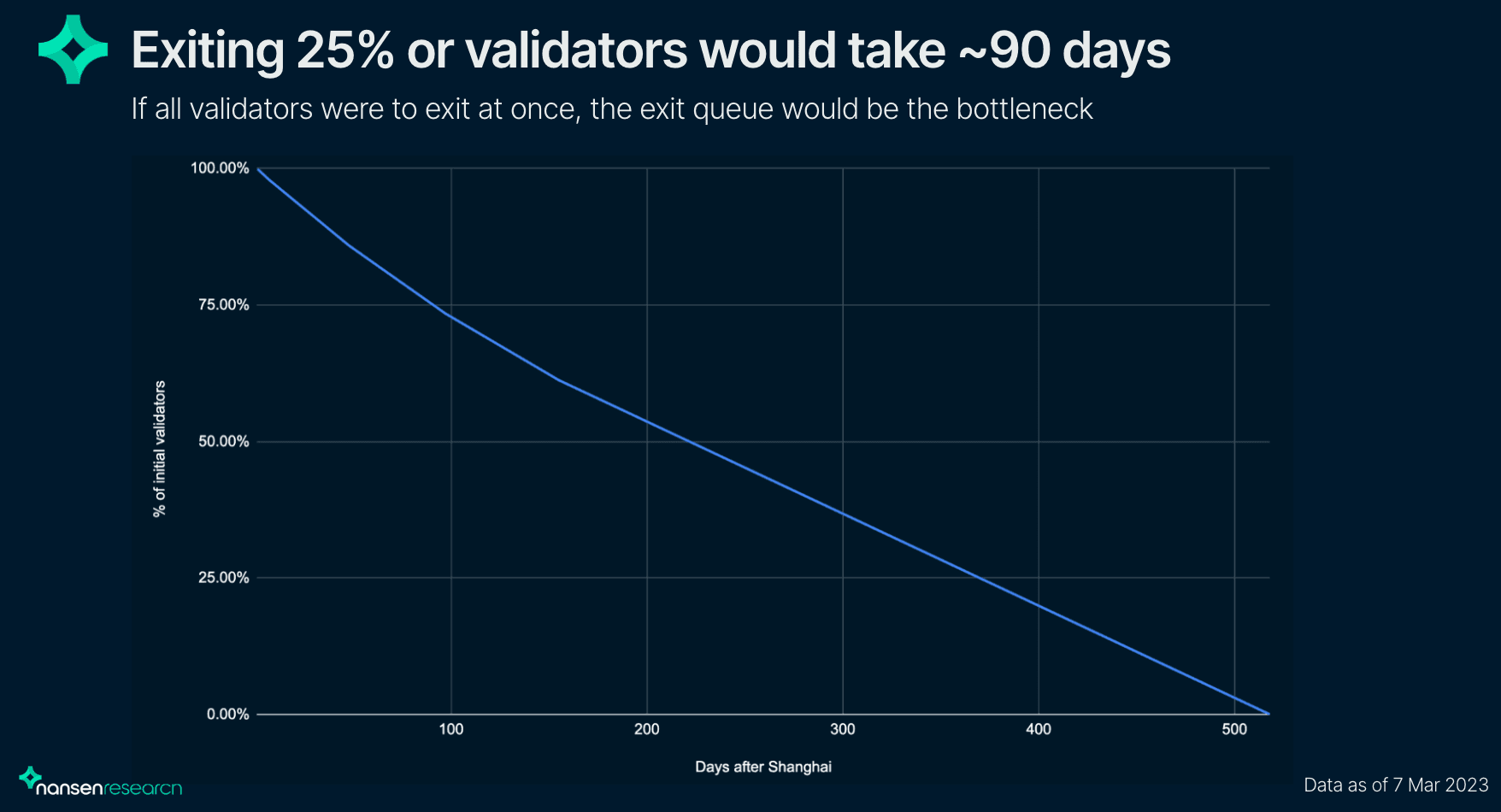

Full voluntary exits (or “full withdrawals”) are a total withdrawal of a validator’s staked ETH. After initiation, full withdrawals are placed in the exit queue after a 4-epoch (6.4 mins per epoch, so ~25 min) delay. Only a limited number of validators may leave the exit queue each epoch (“churn limit”), depending on the current number of validators:

Currently, this would be 1,800 full exits/day. It would theoretically take around 3 months for 25% of all validators to go through the exit queue. This will most likely be the bottleneck for full validator exits.

After validators leave the exit queue, there is another 256 epoch (~27h) withdrawal delay before becoming eligible for withdrawal. Once eligible, they get the chance to be swept and be part of the up to 16 validators, whose withdrawals will be processed in the current block.

Another great article the general workings of unstaking after Shanghai, is this report by Cumberland.

Unstaking-Based Selling Pressure

This section aims to derive a realistic scenario of the potential unstaking-based sell pressure, if/when the Shanghai upgrade is successful.

Staker profiles

This report examines stakers along two dimensions

1. How they staked:

- illiquid,

- liquid centralized or

- liquid decentralized,

2. Whether or not they are in profit.

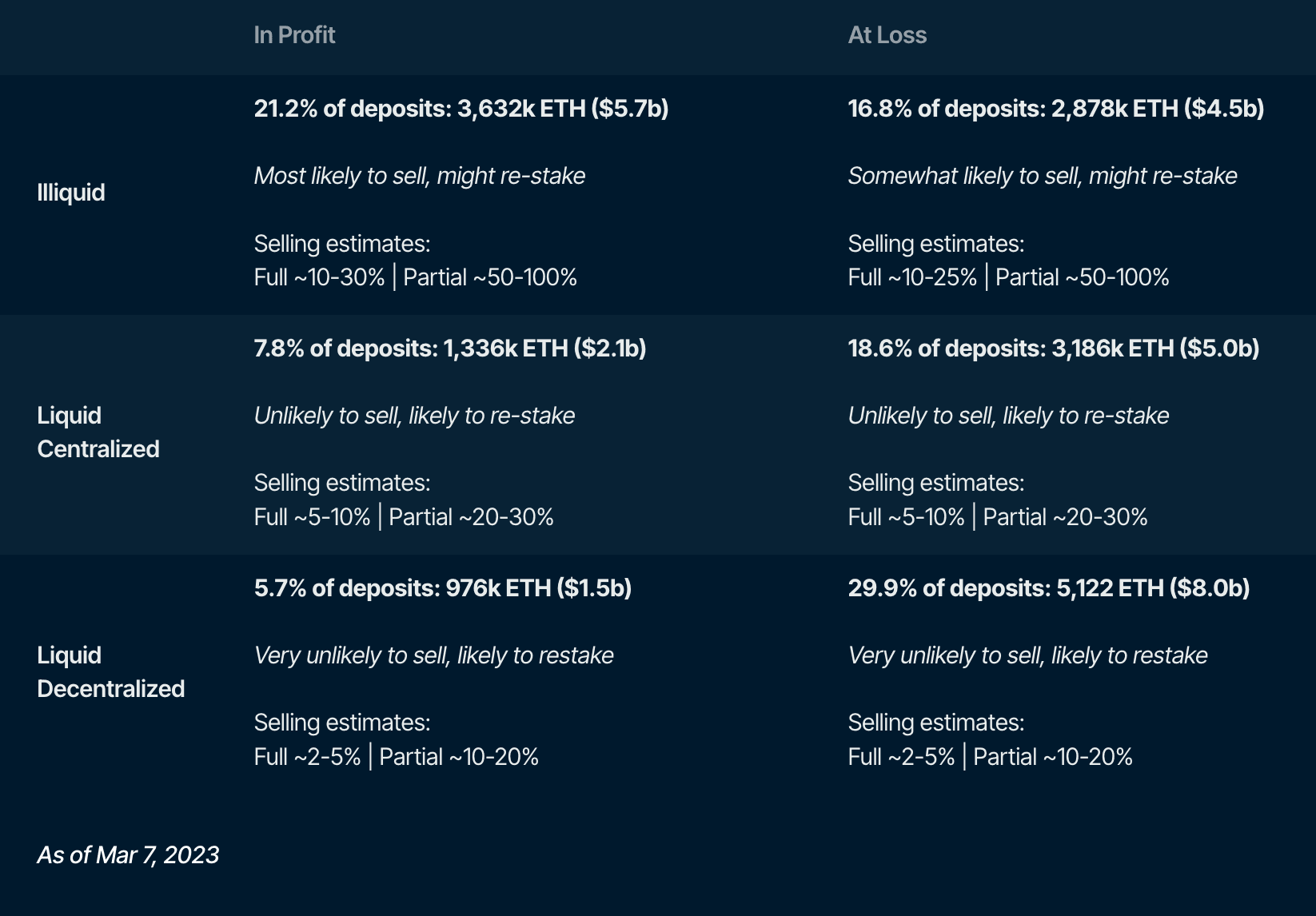

Illiquid stakers

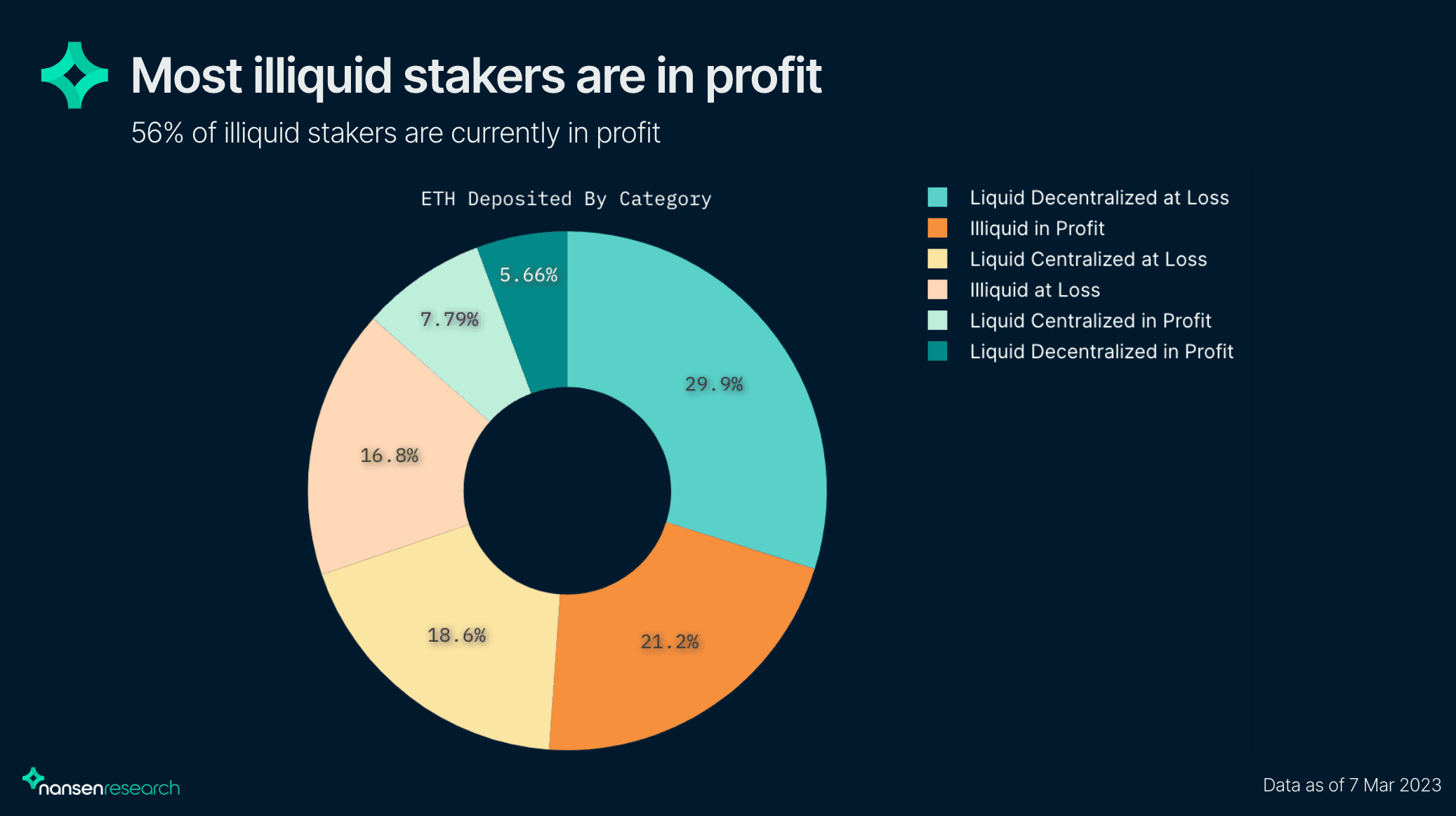

Illiquid stakers account for 38% of total staked ETH. These stakers are most likely to sell after the unlock. Capital has likely been locked for a significant amount of time, as illiquid staking was dominant, especially in the early days of the beacon chain. They might want to sell some of the unlocked ETH for various reasons, which might include:

- Illiquid stakers have on average the highest barrier to restake partial withdrawals, as setting up new validators requires some effort and not everyone might be willing to commit another full 32 ETH (although there is the option to re-stake via other providers).

- Many depositors’ situations may have significantly changed since they first staked, and some may want to reallocate or are forced to sell.

- Most of the illiquid staking deposits are in profit (61%), and they might want to realize their gains, especially after such a difficult 12 months.

Liquid Stakers

Liquid stakers in general are unlikely to sell following Shanghai as they already could have exited their position at any time leading up to the upgrade.

Liquid Centralized Stakers

These stakers are already liquid, so should have no new reason to sell after Shanghai. The staking platforms themselves are also incentivized to re-stake the partial withdrawals, in order to keep their yields competitive.

However, there will likely be some unlocking to redeem the liquid tokens until they very closely track the price of the underlying ETH (“restoring the peg”) which might result in some selling pressure. This would be purely for arbitrage purposes.

In addition, regulators have been cracking down on staking services, and some centralized staking providers might be forced to unstake and distribute the ETH to their clients, some of which might sell instead of staking with another platform.

Liquid decentralized stakers

Liquid decentralized stakers are probably the category least likely to sell upon unlock, for many of the same reasons as centralized stakers. Additionally, there is currently no risk of them being forced by regulators to redeem all tokens to users, making them even less likely to sell after the unlock than centralized liquid stakers. Furthermore, potential DeFi integrations for LSD providers’ liquid tokens can create additional incentives for their users to keep their ETH staked.

Liquid centralized stakers are likely to be less sensitive to being in or out of profit.

Unstaking Selling Pressure Scenario

As explained above, the majority of selling pressure will likely be attributed to the illiquid stakers (38%), especially those in profit (23.3%). Selling pressure from liquid stakers is expected to be almost negligible in comparison.

The table below shows estimates of how much selling pressure each staker profile might create, which will be used to define our scenarios. The probability of not everyone completing the necessary upgrade to a 0x01 withdrawal address is included in the estimated ranges which are likely to be on the more conservative (i.e. pessimistic) side.

NB. Figures are based on an ETH price of $1570. Note this is highly volatile.

Taking all of the above into account, we arrive at a scenario where there is 1.2m-3m ETH (~$1.9-$4.6b) total selling pressure.

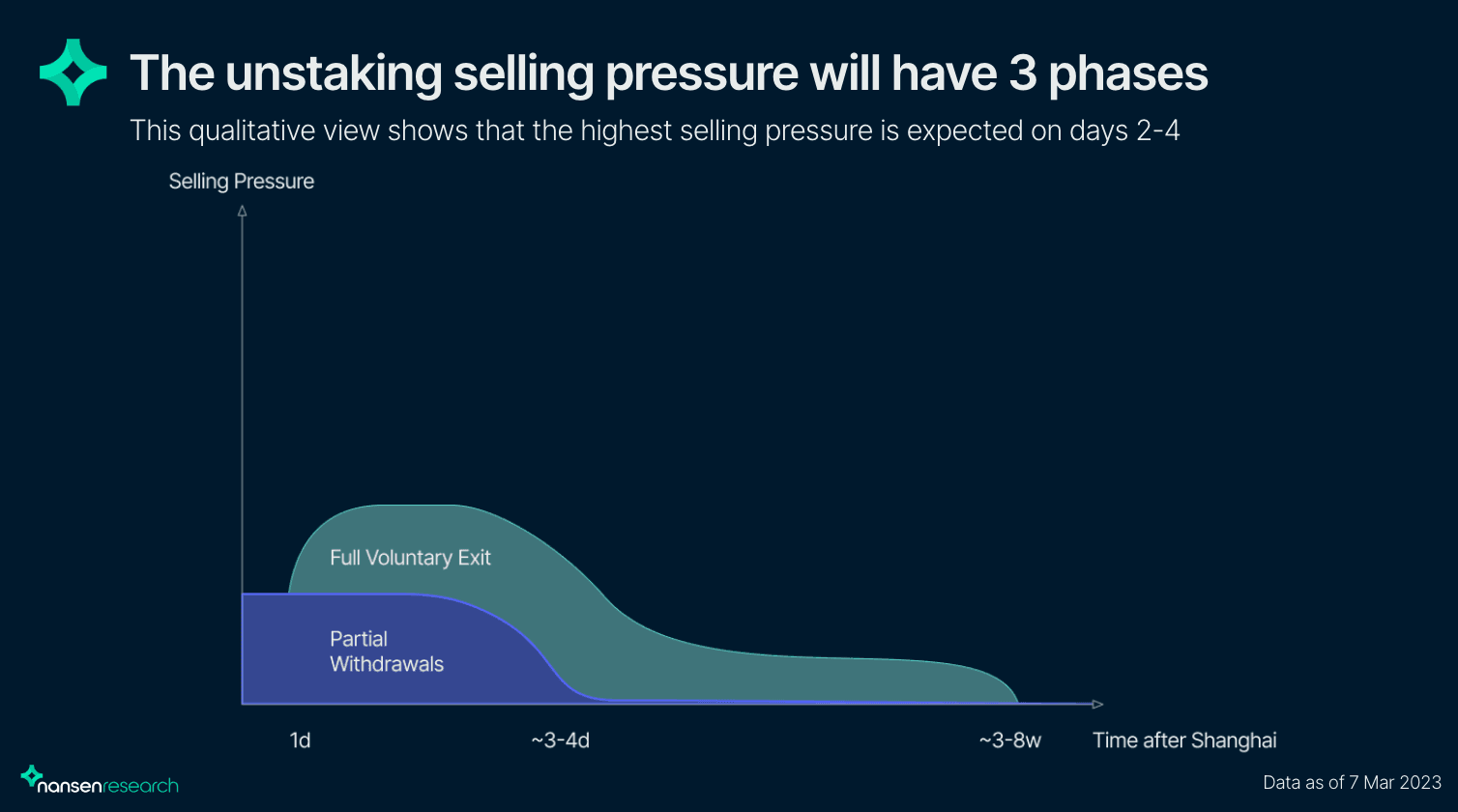

Following the withdrawal mechanics explained previously, the selling pressure from unstaking is likely to occur in 3 phases:

Phase 1 (until ~27h after upgrade): Only partial withdrawal selling pressure due to the withdrawal delay for full exits.

- Estimated additional selling pressure in this period: 84k-125k ETH/day (~$133m - $197m) Phase 2 (until 3-4 days after upgrade): Partial withdrawal selling pressure and full withdrawal selling pressure until all of the initial partial withdrawals have been processed.

- Estimated additional selling pressure in this period: 136k-173k ETH/day (~$218m - $275m)

Phase 3 (until ~19-52 days after upgrade): Withdrawal selling pressure from full withdrawals until all initial full withdrawals have been processed, monitoring the exit queue closely will help to adjust these estimates.

- Estimated additional selling pressure in this period: 48k-53k ETH/day (~$75m - $83m)

The chart below visualizes the scenario described above. This scenario is similar to what other authors like smrti have deducted, albeit with different assumptions.

Other Factors to Consider

Apart from the pure numbers-driven unstaking sell pressure, Shanghai will have several other impacts on ETH spot markets, which are very hard to quantify.

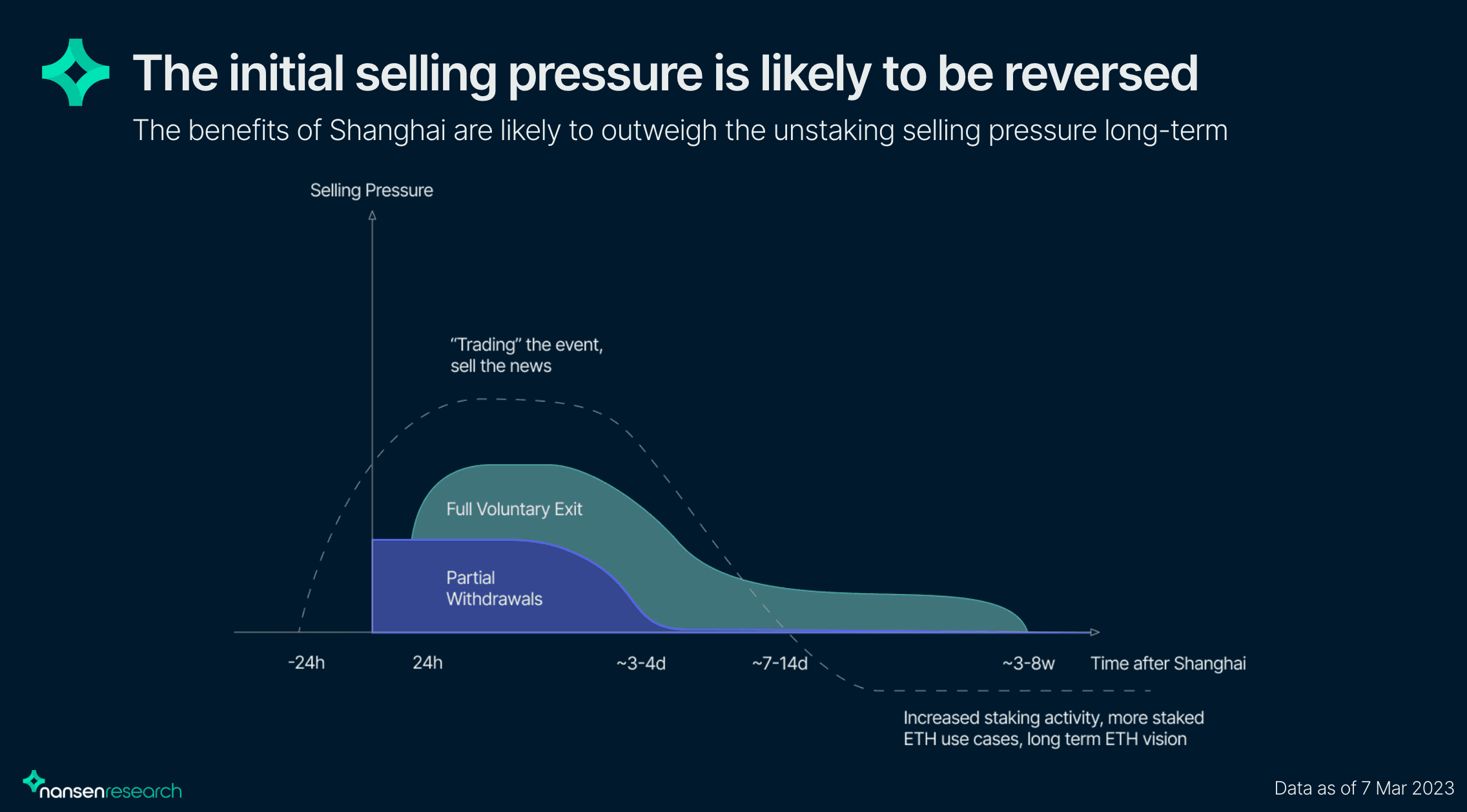

More selling pressure

General trading activities around Shanghai and people trying to “play” the event are other factors, which might increase the selling pressure even further. The behavior of traders going into Shanghai might include:

Sell the news

As with many big scheduled events or upgrades, people like to accumulate well beforehand with the plan to sell into the successful event and make some profits. This “sell the news” phenomenon usually occurs around the time of the actual announcement or even a few hours up to days before. This occurred for the Merge, whereby there was a run-up in price prior to the event but following the successful execution of the Merge, the price of ETH actually dropped.

Front-running sell pressure

Another factor leading traders to sell, is the attempt to front-run the unstaking based selling pressure discussed in the previous section. This would likely be temporary, as those traders will try to buy back at lower prices.

Failed upgrade

Due to extensive testing, this event is highly unlikely. However, there is a non-zero chance of this upgrade failing for one reason or another, and this would likely create heavy selling pressure on ETH. Even without this event actually happening, traders may choose to de-risk before the actual upgrade.

More buying pressure

On the other hand, there are several factors potentially increasing buying pressure. Most of these factors are likely to set in with a slight delay after the upgrade:

Long-term Ethereum vision

A successful upgrade could also lead to overall increased buying pressure beyond the short-term as it is inherently bullish that Ethereum is making progress on its roadmap.

Increased security for stakers

Timely and safe withdrawals may make staking more attractive to more conservative market participants (e.g. institutions). It is likely that LSD providers will see additional inflows of ETH as the 1:1 redemption risk largely vanishes. With Shanghai imminent, staking activity has been at a 6 month high, with only around 1k out of 540k validators waiting to exit, while 4k are pending activation. This is likely to even increase after a successful upgrade, so it is not 100% certain that the number of staked validators will drop in the short-term post Shanghai. In the mid-to-long-term, the number of validators is expected to grow.

ETH has a relatively low staking percentage compared to other PoS chains, and has some room to grow. However, Ethereum is highly unlikely to reach the same staking levels as these other chains. This is because ETH as an asset has value in other ways; such as money (NFTs), collateral, and so on. The utility of ETH as an asset is strong throughout the Ethereum ecosystem and is not purely a staking token.

More use cases for staked ETH

As unstaking becomes more timely and secure, it is probable that there will be more strategies and products incorporating ETH staking. Examples include delta-neutral strategies (stake ETH and short it as a hedge), as well as more integrations of liquid-staked ETH tokens into the larger DeFi ecosystem. This is likely to also introduce a lower yield threshold (i.e. minimum number of staked ETH) above which these strategies become really attractive and people are incentivized to stake. This threshold is depending on market conditions like competing yields, but can potentially create a strong lower resistance for total staked ETH, especially in a low-yield environment.

Bottom-line

Combining all the arguments above, a likely scenario exhibits some selling pressure in the time immediately around the upgrade (1 day before, until around a week afterward), followed by a long-term bullish outlook if the upgrade is successful. This scenario excludes “external” factors like the general macro environment or other non-Shanghai-related news. Below is a depiction of the selling pressure (if positive) and buying pressure (if negative) of this scenario.

As these other factors are hard to quantify, this is a purely qualitative assessment.

Spot Volume and Liquidity

Taking into account that the daily ETH spot volume is around $5b-$6b, the numbers from the purely unstaking driven scenario ($1.9-$4.6b) which are spread over several weeks seem insignificant at first. However, a look into the ETH spot liquidity can provide more insights into the actual impact this selling pressure could have on the price.

According to Kaiko, ETH spot liquidity on centralized exchanges is currently at its lowest levels since the Terra collapse in May 2022 with a 2% market depth is 57,000 ETH - which is half of what it was in October 2022. This does not take into account on-chain liquidity, which would deepen this liquidity.While this can make assets more volatile in both directions, if this thin liquidity remains by the time of the Shanghai upgrade, then the additional sell pressure could indeed be bearish for the price of ETH in the short term.

The short-term selling pressure extrapolated is relatively insignificant compared to the daily volume. However, the market depends on various external factors, and if no additional buying pressure counteracts this it could lead to a notable negative price impact. Note that spot liquidity for ETH is often overestimated. Still, there are several reasons why this counteracting buying pressure might actually occur, especially beyond the short-term.

Despite a potential initial period of net-selling pressure (up to a few weeks), Shanghai means that Ethereum continues to execute its roadmap, enabling the developer community to focus more on its scaling roadmap - which is undeniably a good thing for the long-term success of Ethereum.