With all eyes on the Merge, a few questions are front of mind:

- How to value the hard-forked tokens?

- How is the market positioned?

- How will the new supply/demand dynamic impact pricing, both short-term and long-term?

We attempt to answer each of these questions based on both a technical understanding of market structure and a fundamental view of supply and demand.

Hard-forked token unlikely to retain value long- term, but could have speculative value short term

While the Merge has been generally accepted and understood across the crypto ecosystem from developers to long-term ETH holders, there has been a last-ditch effort to throw a wrench in the works by the ETH mining community, with prominent miner Chandler Guo leading the charge. Guo and the Ethereum miners have proposed to hard-fork the main Ethereum chain, which means continuing a separate copy of the existing ETH network post-Merge, and maintaining it via the existing proof-of- work (PoW) consensus mechanism. Therefore, post- Merge, if you own ETH, you will transition to the proof-of- stake (PoS) ETH, but also receive a newly forked proof- of-work version of ETH (ETH PoW), along with forked versions of ERC-20 tokens.

Will ETH PoW have value even though it’s unlikely to threaten the PoS ETH?

The forked ERC-20 tokens are unlikely to be supported by the major protocols, which would mean the ETH PoW platform is unlikely to have much utility nor underlying value by L1 standards. Nevertheless, this Hail Mary attempt by the miners is not surprising, as a move to PoS puts miners out of business. Many of them have millions of dollars in hardware, and make a good living operating it. When the Merge is complete, the hardware will become obsolete, with all of it coming to market at the same time.

We are skeptical that ETH PoW will gain any traction in the long term.

The Merge is not contentious, and there has not been any serious community pushback aside from the Ethereum miners. This is unlike the Bitcoin Cash (BCH) hard-fork during the Block Size Wars, where a vocal and substantial minority of the BTC community were supportive of the fork. With the market so intensely focused on the Merge, there is a possibility of a brief period of success for ETH PoW, leading to a short-term appreciation of the token value. However, despite the possibility of a short-term rally in the forked token, we are not predicting any material interest from companies, services or protocols to serve the proposed PoW fork. Without a concrete long-term use case, it’s expected that any initial momentum will gradually fizzle. A key opportunity is likely in arbitrage between the different approaches that the various exchanges take to the fork and ETH PoW tokens.

APPENDIX: What is the Merge? The Merge is Ethereum’s long-awaited transition from proof-of-work (PoW) to proof-of-stake (PoS). It is set to occur in mid- to late- September of this year. The goal of moving to PoS is to set the foundations for increased scalability and security.

The Merge has been on Ethereum’s road map since its inception, but now we are finally in the home stretch. All three testnets—Ropsten, Sepolia and Goerli—have now undergone a successful upgrade.

The only remaining event left before the Merge is the Bellatrix update which sets up the Merge on mainnet. This is targeted to occur on September 6, which will set the terminal total difficulty. Once Bellatrix is executed, the prime focus will be around hashpower on ETH.

How is the market positioned going into the Merge?

Futures: Markets implying a successful Merge in September as the most likely outcome

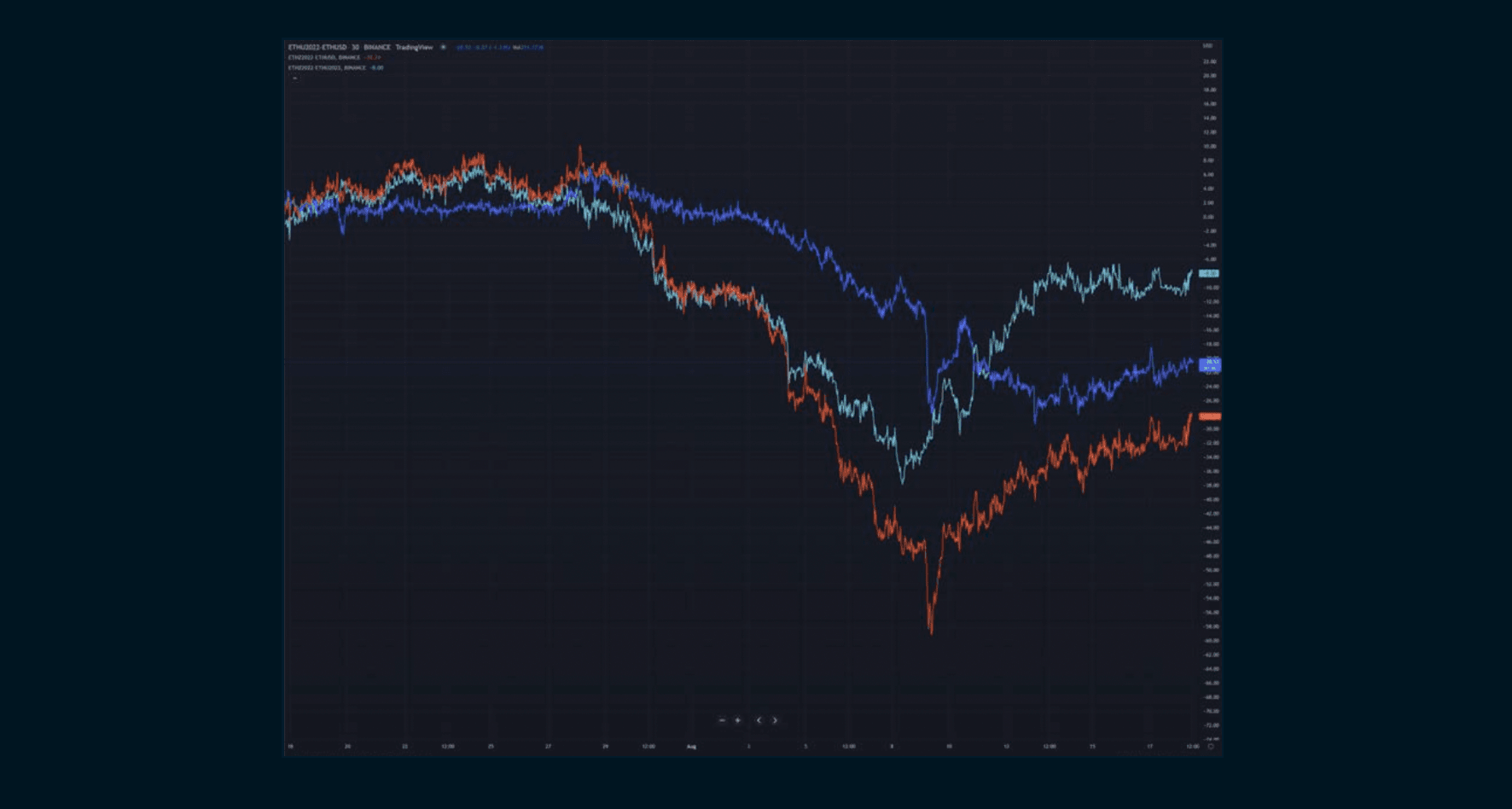

Market participants only receive ETH PoW if they hold spot ETH, and receive nothing if they hold ETH futures. Therefore, we can infer how much the market estimates ETH PoW will be worth from the spot-futures basis. Markets are currently implying ETH PoW to be priced ~$30, which is ~1.5% of ETH market cap. This is slightly lower in comparison to ETC, which is around 2.5% of ETH market cap. However, we do see significant discrepancy in pricing across trading venues

Instead of taking outright ETH price risk, ETH holders have been positioning for the ETH PoW fork via market neutral strategies in the futures market. The typical trade is to buy spot ETH, and sell futures against it. This allows ETH holders to receive ETH PoW without downside price risk. Due to the uncertainty of the Merge date, ETH holders have been selling both the September and December futures contracts.

Initially, selling of December futures seemed to be a safer bet, because sellers of the December basis would still benefit from a successful September Merge. If there were to be any hiccups, price action in the September basis could become chaotic, while the December basis would more likely retain value. As of August 17, 2022, the September spot-futures basis is ~$23 while the December is ~$30. However, as a September Merge date becomes more likely, the futures discount has concentrated in September.

The extent to which the spot-futures basis trade is impacting the market is best illustrated in the recent change in the shape of the futures curve. As a result of funding costs, ETH calendar spreads typically trade in contango (positively-sloped). However, due to the volume of selling that has taken place in the less liquid longer dated contracts, the curve has twisted into backwaration (negatively-sloped). It remains to be determined how long the curve will retain this shape. Based on the current price of spot ETH and growing likelihood of the Merge taking place in September, it is possible this will only persist in the short term.

Overall, the wide acceptance of the transition to PoS suggests that the basis trades will be liquidated quickly post-Merge after ETH Holders have received their ETH PoW. This market anomaly will not persist for long post- Merge, especially if the Merge proves successful and stokes a broader rally.

Options: ETH vol dominating BTC vol with the Merge acting as a catalyst while BTC lacks clear macro direction

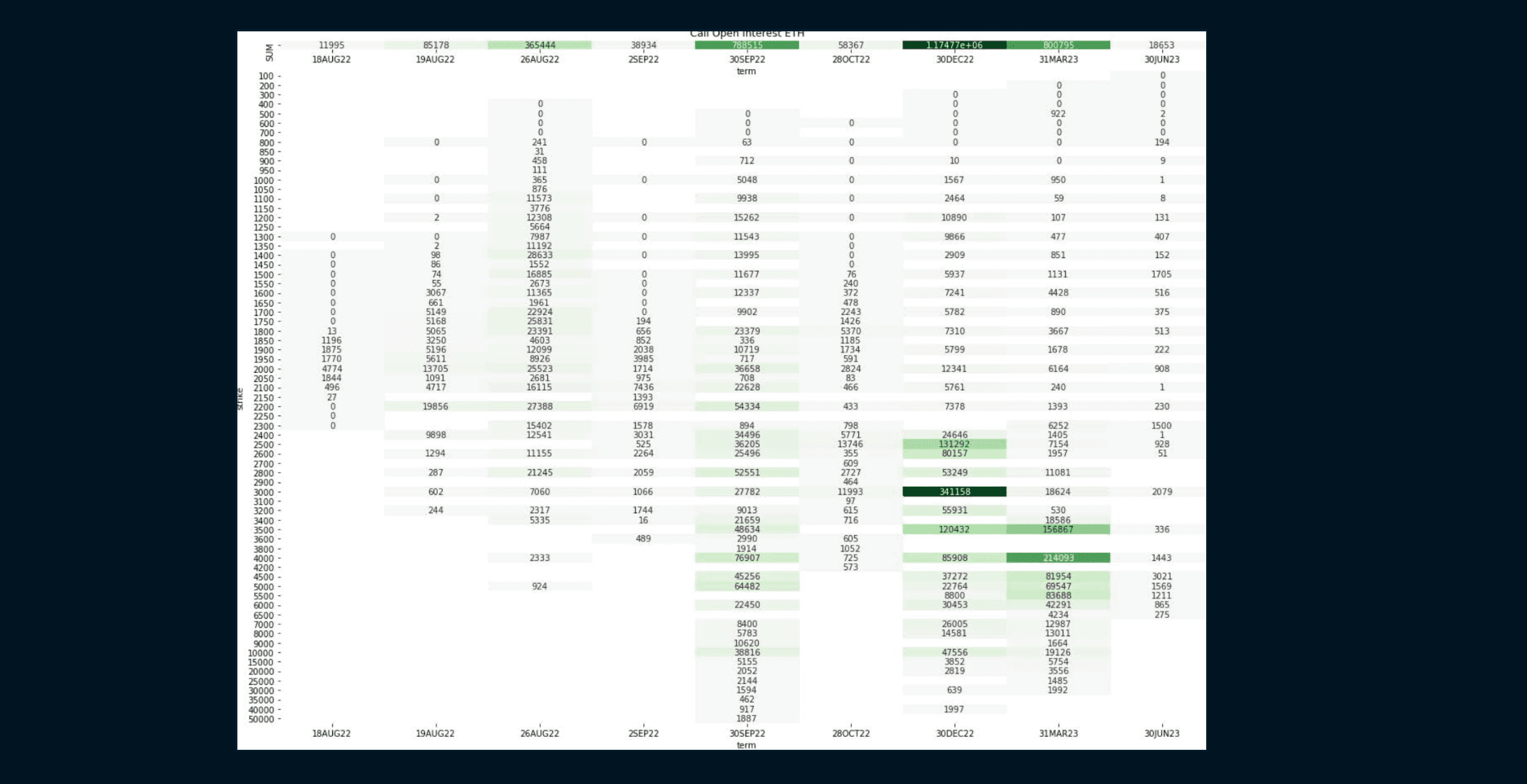

Since the Q2 2022 sell-off, market participants have been reluctant to redeploy capital into risk assets until the interest rate outlook is more certain. Instead, we are seeing many market participants using options strategies to express their views on the Merge in ways that limit their downside exposure. As a result, for the first time we have seen open interest of ETH vol outpace that of BTC vol in terms of notional value.

The majority of the structures we have seen in ETH options have been upside call-spreads, call-flies and outright call options. This flow has pushed the “BTC vol to ETH vol” ratio to the lower end of its historic trading range of 60-95%. Currently, the ATM September 30 ETH vol is slightly above 100% and the BTC/ETH vol ratio is slightly below 70%. This is implying about a 1.5x outperformance of ETH vs BTC per 1 SD move on the Merge. Given that it’s such a high-variance event, we view these levels as a fair price for ETH vol.

In addition, the potential post-fork unwind of the previously discussed spot vs futures trades will likely lead to further short-term volatility, which is also being captured in these vol levels. However, the market does expect diminished volatility post-Merge. While the term structure is increasingly steep into September due to the Merge, vol is downward sloping following the September option expiry.

From the open interest heatmap below, most of the bullish strategies have been expressed as butterflies in and around the $3K level. Using the $2500-3000-3500 butterfly in December 30 expiries for example, it implies that market participants are targeting $3000 ETH for maximum profit. It’s important to acknowledge that as ETH rallies, options market makers will begin to derive shorter gamma as the price of ETH approaches the first strike around $2500. Therefore, should spot approach that level prior to the options expiring, there will likely be sharper moves higher in both ETH Vol and spot ETH as market makers hedge their risk.

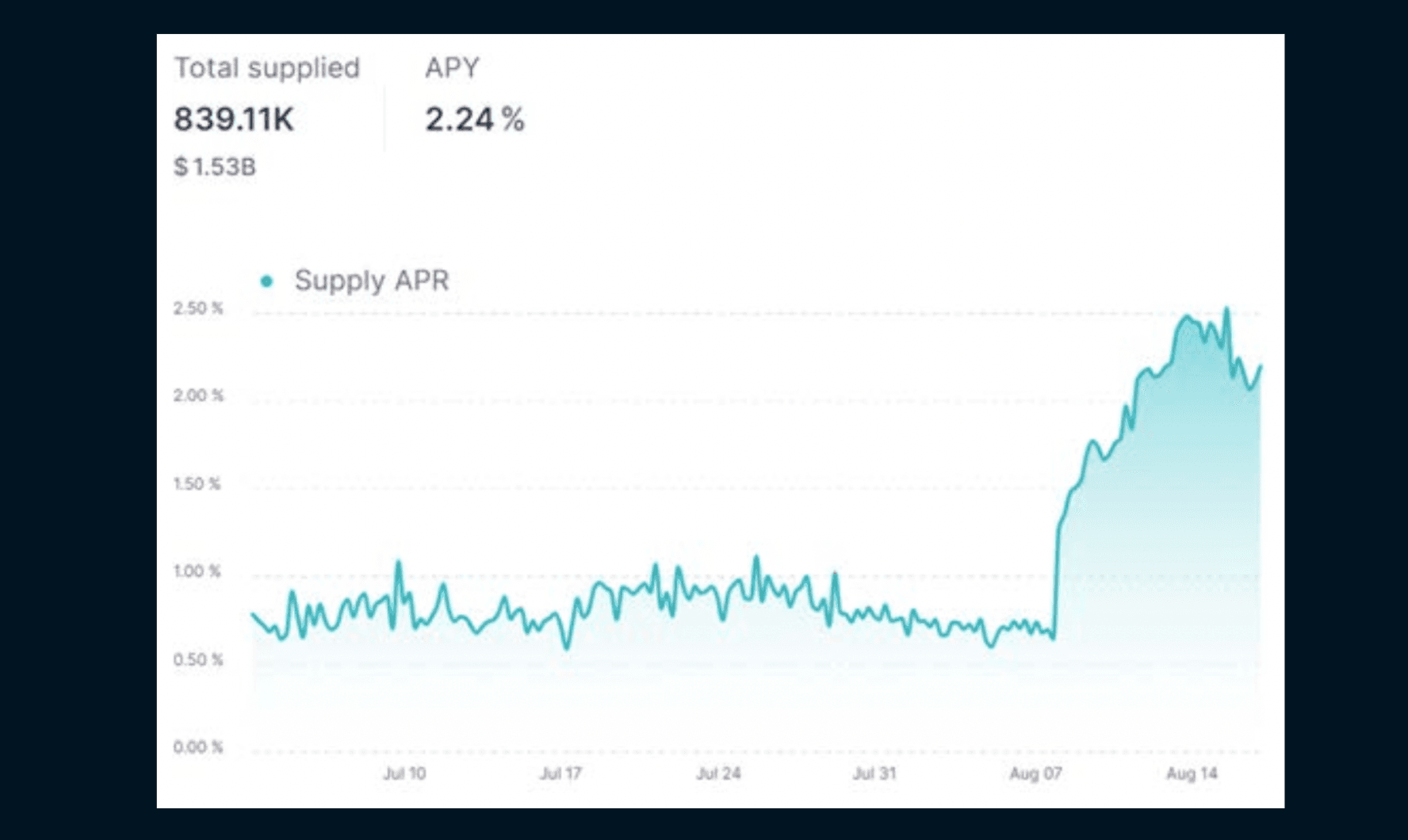

DeFi: The fork is also distorting borrowing rates

The fork is also creating distortions in DeFi borrow markets, where market participants are borrowing ETH in order to receive ETH PoW. As long as the borrow rates paid is lower than the value of the ETH PoW received, it’s profitable to borrow more, pushing up borrow rates further. If rates are not sufficiently high, it will also result in borrowing pools being 100% utilized, which prevents lenders from withdrawing.

Short-term Supply & Demand: Selling pressure from miners disappearing likely bullish

There are two short-term factors to consider:

Supply and Demand – The price of ETH since the Luna crash has been trading in a well-defined range of $1000-$2000. This price has held well despite an estimated $40mm of daily miner selling, which implies there is equally about $40mm of daily buying demand. Assuming the ETH PoW fork does not lead to a robust new market, it is safe to assume that this $40mm of daily selling will disappear once the PoS chain is established. With the demand persisting, and the supply decreased due to the Merge, we would expect upward price pressure to resume. This should ultimately look very similar to the halving of the miner rewards, which have typically been followed by bullish price action.

Staking – Staked ETH will remain locked-up until a future date, when the next Ethereum Improvement Proposal releases them (EIP-4788). While the implementation date is currently unknown, we do know that 13.2m ETH or ~$21bn of ETH will be eligible to be withdrawn. Of course, it's unlikely that all of the currently staked ETH will become unstaked. Furthermore, even if all the staked ETH were to be unstaked, there will be a queue which on average would take about 6 months for all the unstaking to be processed. This potential unlock could weigh on the market until there is more certainty around the actual amount of ETH to be unstaked and sold. The unstaking is essentially the event to "sell-the-fact" rather than the actual Merge, which, if successful, should reprice ETH higher as miner supply is reduced.

The long-term view on ETH post-Merge

Despite the conflicting factors noted previously that will likely create some uncertainty in the short-term, we feel confident that the Merge will ultimately lead to upward price pressure over the long-term. Adding to our conviction is the growing interest we’ve seen in various bullish options strategies and the dry powder in the form of substantial cash positions following the recent deleveraging of the market.

Overall, we expect to see effective supply fall by about 95% while staking demand increases post-Merge. Our positive long-term view is based on the following factors:

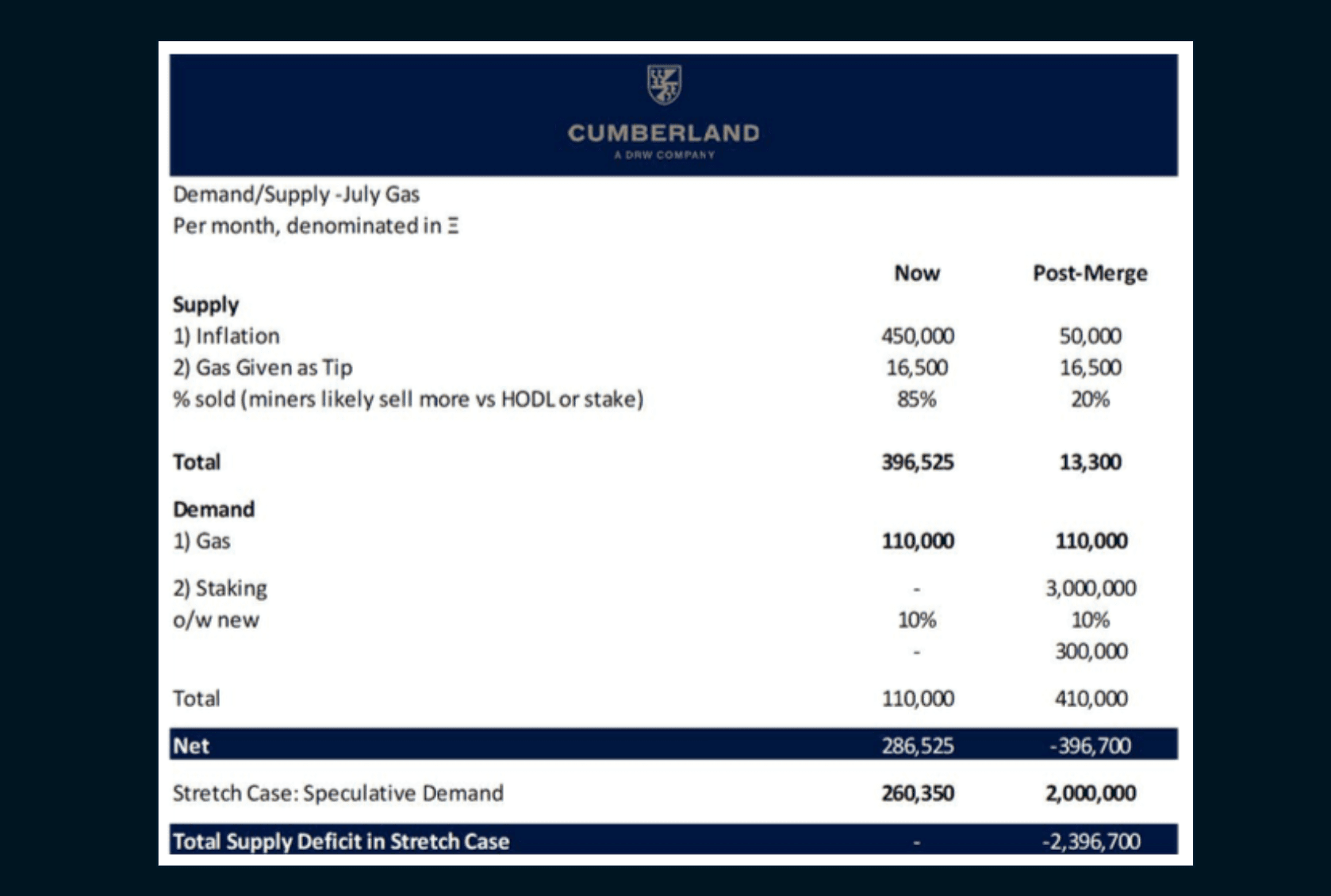

- On the supply side, we see gross inflation falling by ~90% and the ~15% of gas paid to miners/stakers as tip remaining stable. However, effective supply should decline by over 95% since we believe miners sell around 80-90% of mined ETH, whereas we very roughly estimate stakers will only sell ~20% due to substantially lower operating costs.

- On the demand side, there are three components:

- Gas: Currently ~110k ETH per month, with ~85% of which being burned. We assume this remains stable post-Merge, though we think this estimate could be conservative.

- Staking Demand: Staking in ETH is currently negligible, with the likely cause being that stakers are holding off until post-Merge given the potential technical risk and uncertain timing. Currently, only around 11% of the total supply is staked, which is significantly below the 50-80% average across major PoS L1s. Assuming a conservative total staked ratio of 60%, this could mean an additional 60m of staked ETH at the current supply of ~120m tokens. A reasonable timeframe for this target to be reached is around 16 to 20 months. Although most of this staking demand will end up coming from existing ETH holders, we do expect around 10% net new stakers, attracted by yields that are expected to be above 5%.

- Speculative Demand: While this is very difficult to estimate, in previous bull markets we have generally seen ~2m ETH per month move from long-term to short-term holders.

Therefore, even without any pick-up in speculative demand, we see the supply/demand balance moving from the current situation of slight excess supply to moderate excess demand. This translates to moving from ~260k ETH per month needing to be absorbed by speculative demand, to an excess demand of ~400k ETH per month. This estimate is likely conservative given current cash levels. There is considerable upside to this if the Merge narrative leads to a sustained pickup in speculative demand. Against this backdrop, around 75% of current supply has not changed hands for around three months. In other words, these tokens are in the hands of quasi long-term holders, which further compounds any potential supply squeeze implied by the below analysis.

Summary: Long-term, this upgrade has high impact.

The ethereum network will have better economic incentives and more validators, setting the foundation for future scaling upgrades. ETH issuance can potentially become deflationary in times of high demand. Sell-pressure from miners, who typically sell 80-90% of their rewards to cover high energy costs, is expected to drop considerably due to the elimination of overhead and energy costs. Overall, even absent a material pickup in new speculative demand, we see the market transitioning from flat/oversupplied to materially undersupplied.